Comparison of Some Brazil and Mexico ADR Rotation Strategies

A B S T R A C T

This study evaluates a

median sector rotation strategy using American Depositary Receipts (ADRs) from

Brazil and Mexico during 2014-2024, a period shaped by tariff shocks and policy

uncertainty. Unlike momentum-driven approaches, the median strategy systematically

avoids extreme sector performers, aiming to reduce volatility and drawdowns for

retail investors. Portfolios were tested under five rebalancing

frequencies—weekly to annual—using total returns, Sharpe ratios and maximum

drawdowns as evaluation metrics. Results indicate that monthly and semi-annual

rotations deliver favorable risk-adjusted performance, particularly during

heightened market turbulence. The findings suggest that median-based allocation

offers a pragmatic, accessible mechanism for individual investors to achieve

stability and moderate growth without reliance on predictive models or advanced

data infrastructure. Keywords: Trading strategies, Momentum strategies, Median

sector rotation, Emerging markets, ADRs, Portfolio rebalancing, Retail investor.

1. Introduction

With pockets of war occurring along with looming threats of

global markets closing, retail investors in emerging markets face

growing challenges amid rising macroeconomic uncertainty,

global trade tensions and volatile capital flows1,2. In countries

such as Brazil and Mexico, inflationary pressure, currency

instability and shifting tariff regimes have introduced heightened

risk exposure across equity markets3,4. Traditional passive

strategies, such as broad index investing, offer diversification

but leave public investors fully exposed to systemic shocks as

seen from the recent drastic drop of the S&P500 early 20253. At

the same time, most sophisticated factor-based or momentum

driven models remain out of reach for non-institutional investors

due to their complexity and data demands5,6

This paper investigates

the application of a median sector rotation strategy-a simple, rule-based

method that reallocates capital to sectors with moderate recent performance-as

a low complexity, risk-mitigating approach for the public. Building on prior work

in the U.S., India and Japan7, we extend the strategy to Latin American

markets, using U.S.-listed ADRs as sectoral proxies. ADRs offer exposure to

Brazilian and Mexican equities through U.S. dollar-denominated instruments,

reducing the impact of currency fluctuations and improving accessibility and

liquidity for retail investors8.

Rather than targeting outperformance through

predictive signals, the median strategy acts as a volatility filter by

systematically avoiding the most extreme sector movement, acting as a

conservative investment for retail investors9. Given

2. Motivation and Context

In emerging markets like Brazil and Mexico,

most investment decisions are influenced by a combination of policy

uncertainty, currency pressure and trade-related shocks, often closely tied to

the US market1. These influences have contributed to uneven performance across

sectors, with trade-heavy industries reacting sharply to changes in tariffs,

inflation or capital flows. For both institutional and retail investors, this

environment raises a practical concern: how to can you invest without taking on

unnecessary risk in sectors most exposed to external disruptions2.

Passive

strategies, while easy to implement, offer little room to adjust for concentrated

risks that emerge in unstable macro conditions. At the same time, active models

often depend on forecasting tools or data infrastructure that most retail

investors can’t access or apply consistently. This leaves a gap between

accessibility and adaptability that few strategies manage to bridge4

A more pragmatic approach

may be to sidestep the extremes. The median sector rotation strategy does this

by reallocating capital to sectors that sit in the middle of recent performance

rankings. It foregoes top performers and chronic underperformers. And instead,

it aims to reduce overall volatility by focusing on more stable segments of the

market (?). This can be particularly useful during periods when sector-level

performance is driven more by policy headlines – as seen from Trump’s recent

introduction of tariffs – than by fundamentals.

The current backdrop adds

weight to this idea. Since early 2025, new U.S. tariffs targeting Brazilian and

Mexican exports especially steel, agricultural products and manufactured

goods-have triggered sharp market reactions3. These trade actions, alongside

weakening local currencies and rising prices, have made returns more erratic

and sector dispersion more pronounced. In this context, a basic rotation

strategy that f ilters out the outliers may offer a degree of protection

without requiring predictive models or high-frequency trading10.

To evaluate

this, the study uses American Depositary Receipts (ADRs) as sector proxies.

ADRs trade in U.S. dollars and offer retail investors simpler access to

international equity exposure with fewer currency-related complications8. We

test the median strategy across different rebalancing cycles and compare its

outcomes with approaches that emphasize either the best- or worst performing

sectors. The goal of our paper is to understand whether a structured yet simple

method of investing using medians can provide a useful buffer in markets where

volatility is becoming a constant.

This work contributes to the broader

conversation about building accessible, data-driven investment frameworks that

can adapt to instability without overcomplicating execution and providing

accessibility for retail investors that do not have the resources to engage

experts2. It focuses on what can be done with basic return data-no forecasts,

no proprietary inputs-so that individual investors have a clearer path forward

in uncertain times.

3. Methodology.

3.1. Sector selection and

Data sources

To evaluate the effectiveness of the median sector rotation

strategy in a Latin American context, we constructed investment portfolios

using American Depositary Receipts (ADRs) representing key sectors from Brazil

and Mexico - the only two countries that had enough ADR based on our threshold

of more than 10 ADRs. ADRs were selected based on liquidity, sectoral

representation and data availability on U.S. exchanges. This approach provides

public investors with U.S. dollar denominated access to Latin American equities

while minimizing friction from local brokerage access, currency volatility and

data opacity (we forego including the cost of trading these ADR with the

assumption that investors would absorb a similar fee in purchasing other

investment products) (Table 1).

|

Ticker |

Name |

Industry

Sector |

|

SID |

Companhia Siderurgica Nacional |

Steel/Basic materials |

|

GGB |

Gerdau S.A. |

Steel/Basic Materials |

|

SBS |

Companhia de Saneamento Basico

do Estado de Sao Paulo |

Utilities |

|

SUZ |

Suzano, S.A. |

Paper |

|

VALE |

Vale S.A. |

Metals/Mining |

|

PBR |

Petroleo Brasileiro

S.A. - Petrobras |

Oil and Gas |

|

ITUB |

Itau Unibanco Holding

S.A. |

Banks |

|

BAK |

Braskem S.A. |

Chemicals |

|

BBD |

Banco Bradesco S.A. |

Banks |

Table 2: List of Maxico ADRs.

|

Ticker |

Name |

Industry

Sector |

|

AMX |

America Movil |

Telecom |

|

ASR |

Grupo Aeroportuario

del Sureste |

Airports |

|

CX |

CEMEX |

Building Materials |

|

FMX |

Fomento Economico Mexicano |

Beverages |

|

KOF |

Coca-Cola FEMSA |

Beverages |

|

OMAB |

Grupo Aeroportuario

del Centro Norte |

Airports |

|

PAC |

Grupo Aeroportuario

del Pac´ıfico |

Airports |

|

SIM |

Grupo Simec |

Steel |

|

VLRS |

Controladora Vuela Compan´ıa de Aviacion |

Airlines |

These sectors were grouped into broader economic categories

using Global Industry Classification Standard

(GICS) mappings. From each country, we selected between 7 to 10 ADRs representing distinct economic

sectors to ensure a balance between coverage

and data quality.

Daily closing prices were collected from Yahoo Finance

and other public financial APIs covering the ten-year period 2014-2024, a

timeframe that includes both stable conditions and periods of macroeconomic

disruption, including trade policy shocks and inflation surges.

3.1.

Portfolio construction and Sector ranking

Following the methodology established in prior studies, sectors were

ranked by total return over a fixed rebalance interval. For each period,

sectors were categorized into the following portfolios:

• Winner Portfolio - Top 3 ADRs by return.

•Loser Portfolio

- Bottom 3 ADRs by return.

• Median Portfolio

- Middle 3 ADRs by return.

Let us consider a simple

numerical example. The initial amount of investment for each group

is set at $100. The trading

strategy for annual rebalancing is to look at previous years sorted returns

and invest in winners, median

and losers. Suppose that the 2014 returns

of ADRs in increasing order

are as follows:

For 2015, the “Winners”

strategy is to invest equally in (BBB, ITUB, SUZ). The “Median” strategy would

be to invest equally in (BAK, SBS, VALE) stocks. Finally, the “Losers” strategy

would be to invest equally in (PBR, GGB, SID) stocks.

3.3.Rebalancing

frequencies

To assess how timing

influences strategy performance, we tested five rebalancing intervals:

• Weekly

•Monthly

•Quarterly

•Semi-Annual

•Annual

This design allows us to

evaluate whether the median strategy’s advantages hold under both high frequency

and low-frequency reallocation regimes.

3.4.Performance evaluation metrics

We

evaluated each strategy using both absolute and risk-adjusted

metrics:

• Final portfolio

value: Ending value after compounding

returns.

• Annual Return.

• Annual

volatility: Standard deviation of returns.

• Tracking error: Difference from benchmark B&H

performance.

•Maximum drawdown

(MDD): Largest observed

peak-to- trough decline.

•Sharpe

ratio: Risk-adjusted return.All metrics were computed

using Python and the empyrical library (Package). Returns were calculated in

U.S. dollars, consistent with the ADR pricing

convention and dividends were excluded to preserve comparability across listings.

3.5.Key assumptions and Limitations

•Transaction

costs: As mentioned, we assumed that purchasing

other investment product will have a similar transaction cost hence in this

paper we assume that the transaction cost is irrelevant.

•Survivorship

bias: We mitigated this by using ADRs that had remained continuously listed

through the 2014–2024 window.

•Sector drift: Given

theADR format, the sector classifications should remain

stable; however, we recognize the limitation

of not capturing smaller or non-U.S.-listed regional

players.

4.Results and Findings (Mexico

ADR Sector Rotation)

4.1Performance by rebalancing frequency

The rotation strategy performance exhibits noticeable variation

depending on the rebalancing frequency, as highlighted by the cumulative cash values and maximum drawdown

(MDD) metrics.

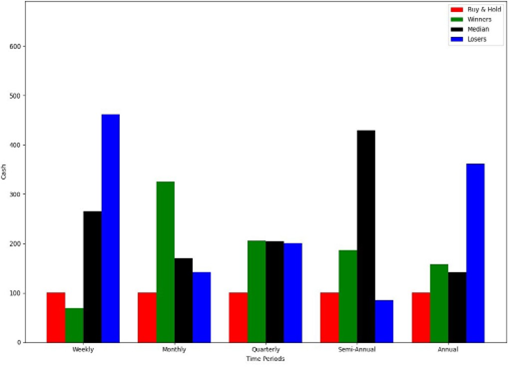

Cumulative Cash Values The cumulative terminal

values (in units of initial capital)

demonstrate that the choice of rebalancing

frequency strongly influences portfolio growth potential. As shown in (Table 3) annual rebalancing yields

moderate results, with the Winners

portfolio growing to 193 and the Median and Losers portfolios reaching 233

and 248 respectively, all outperforming the Buy-and-Hold baseline of 101.

Increasing the rebalancing

frequency to Semi-Annual and Quarterly notably improves performance for some

groups; for example, the Median portfolio achieves its highest terminal value

of 345 under Semi-Annual rebalancing, while the Losers portfolio peaks at 432

under Quarterly rebalancing. Monthly rebalancing provides the highest growth

for the Winners portfolio (319), suggesting that adapting portfolio weights more

frequently can better capture momentum effects.

Interestingly, the Losers portfolio does not uniformly

decline but occasionally achieves

strong growth (e.g.,

432 at Quarterly), indicating potential profit opportunities even

among previously underperforming ETFs if rebalancing is frequent enough.

Weekly rebalancing results in

respectable but not always superior cumulative values compared to Monthly or

Quarterly, hinting at possible diminishing returns.

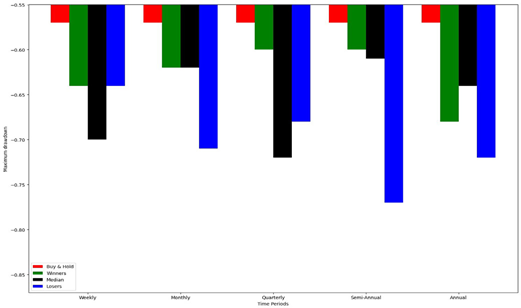

Maximum Drawdown

(MDD) The MDD analysis reveals

the downside risk accompanying each rebalancing frequency. Lower (less negative) MDD values indicate

better capital preservation.

As shown in (Figure 2) Annual and Semi-Annual frequencies

produce

generally lower drawdowns for the Winners portfolio (around -0.60 to -0.68),

reflecting a balance between return and risk.

The Median and Losers portfolios experience slightly larger drawdowns, especially under higher

frequencies like Quarterly and Weekly, where MDD ranges from -0.62 to -0.77.

The Buy-and-Hold strategy,

despite its relatively low returns, displays the smallest drawdown (-0.57),

demonstrating its conservative risk profile.

The results underscore the

classic trade-off: more frequent rebalancing can enhance returns by exploiting

changing market momentum but may increase volatility and susceptibility to

deeper drawdowns.

Summary: the cash values and

MDDs across different rebalancing intervals illustrate clear performance and

risk trade-offs. Monthly and

Quarterly rebalancing frequencies appear to offer favorable combinations of

growth and control over downside risk for Winner’s portfolios, while less

frequent rebalancing such as Annual or Semi-Annual may appeal to investors

prioritizing lower volatility. These findings can guide practitioners in

calibrating rotation strategies to their risk tolerance and market outlook.

4.2.Performance by rebalancing frequency: Mexico portfolio

The rotation strategy

applied to Mexican

ETFs demonstrates significant

variation in performance and risk across different portfolio rebalancing

frequencies, as seen through cumulative cash values and maximum drawdown (MDD)

statistics.

Cumulative Cash Values The

terminal portfolio values indicate that rebalancing frequency has a marked impact on portfolio growth potential. As

shown in Table 4 Annual rebalancing delivers modest growth, with the Winners

portfolio reaching 157 and the Median and Losers portfolios at 142 and

362 respectively, all exceeding the baseline Buy-and-Hold value of 100.

Semi-Annual rebalancing

markedly boosts the Median portfolio’s terminal value to 429, reflecting that less frequent

but regular adjustments can sometimes better

capture medium-term momentum.

Quarterly rebalancing also improves the Winners portfolio (206), while Monthly

rebalancing produces the most substantial growth in the Winners

group (325), confirming that more frequent portfolio

updates can intensify returns by exploiting recent performance trends.

Notably, the Losers portfolio

shows strong terminal values under Annual (362) and Weekly (461) rebalancing, which

suggests unique market behaviors or opportunities for reversal strategies among

underperforming Mexican ETFs.

Weekly rebalancing results are mixed, showing

high returns for the Losers group but significantly lower performance for Winners (69), indicating potential

risks or inefficiencies associated with very short-term rotation.

Maximum Drawdown (MDD) The MDD values highlight the

downside risks inherent in each rebalancing frequency. As shown

Median portfolios

experience their lowest drawdowns around

-0.48 annually and -0.55 with

weekly adjustments, showing relative stability in moderate performers. Losers

suffer larger drawdowns in most cases, particularly under Semi-Annual and

Weekly rebalancing (-0.70 and -0.68), revealing increased risk in frequently

rotated underperformers.

The Buy-and-Hold approach,

while generating the least returns, maintains a stable and moderate drawdown

(-0.54), underscoring its conservative nature.

Summary: The Mexico portfolio

results underscore the trade-offs between return

enhancement and risk control inherent in choosing a rotation

frequency. Monthly rebalancing excels in delivering superior growth with the lowest drawdowns for Winners, whereas Semi-Annual

rebalancing significantly benefits Median portfolios. Annual and Weekly

frequencies display divergent results particularly for Losers, highlighting

market-specific effects (Figure 1).

These insights assist investors in tailoring rebalancing strategies according

to their risk tolerance and desire for return maximization in the Mexican ETF market (Tables 3 and 4).

Table 3: Brazil: Comparison of Strategies Final Balances for Different Rotation

Frequencies.

|

Strategy |

|

ROTATION

FREQUENCY |

|

||

|

Annual |

Semi-Annual |

Quarterly |

Monthly |

Weekly |

|

|

Winners |

193 |

257 |

277 |

319 |

253 |

|

Median |

233 |

345 |

97 |

248 |

187 |

|

Losers |

248 |

137 |

432 |

146 |

247 |

|

Buy & Hold |

|

101 |

|

||

Table 4: Mexico: Comparison of Strategies Final Balances for Different Rotation Frequencies.

|

Strategy |

|

ROTATION

FREQUENCY |

|

||

|

Annual |

Semi-Annual |

Quarterly |

Monthly |

Weekly |

|

|

Winners |

157 |

186 |

206 |

325 |

69 |

|

Median |

142 |

429 |

204 |

170 |

265 |

|

Losers |

362 |

86 |

201 |

143 |

461 |

|

Buy & Hold |

|

100 |

|

||

Figure 1: Brazil Comparing cash across various strategies and frequencies.

5.Conclusion

The median sector rotation strategy

provides a robust, low-complexity approach to navigating volatile emerging

markets impacted by policy shocks. Monthly and semi-annual rebalancing optimize

the balance between returns and risk. By avoiding extremes, this method offers

retail investors (Figures 2-6).

Figure 2: Brazil Comparing maxdrawdowns across various

strategies and frequencies.

Figure 3: Mexico Comparing cash across various

strategies and frequencies.

Figure 4: Mexico Comparing maxdrawdowns across various

strategies and frequencies.

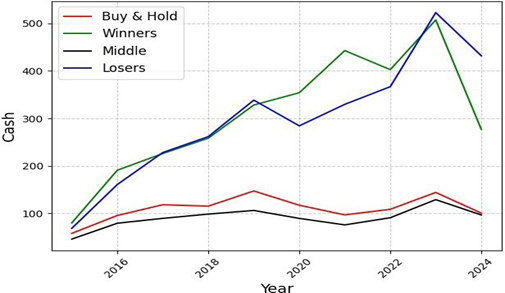

Figure 5: Brazil’s best investment strategy.

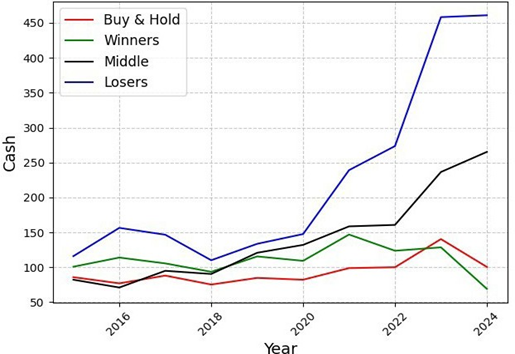

Figure 6: Mexico’s best investment strategy.

A practical alternative to

active forecasting models, enhancing stability without sacrificing growth

potential during periods of heightened uncertainty, such as those triggered by

recent U.S. tariffs on Latin American exports.

6.Acknowledgements

6.1.Conflict of interest

We declare that there are no conflicts of interest regarding the

publication of this paper.

6.2.Author contributions

All the authors contributed equally to the effort.

6.3.Funding

This research was conducted

without any external funding. All aspects of the study, including design, data

collection, analysis and interpretation, were carried out using the resources

available within the authors’ institution.

6.4.Data Availability (including Appendices)

All the relevant data, Python code for analysis, detailed annual

tables and graphs are available via: https://github.com/ traders2025/Rotation_Strategy_Brazil_Mexico/tree/main

7.References

- Alexiou C, Tygi A.

Gauging the effectiveness of sector rotation

strategies: Evidence from the u.s. and europe.

Journal of Asset

Management, 2020.

- Johnson AL. ETF Strategy: Sector Rotation. Wiley,

2024.

- Phillip C, Kim I, Cheh J. Sector rotation and interest rate policy.

International Journal of Business and Social

Research, 2014.

- Nadler D, Schmidt A. Momentum strategies for

etf-based portfolios. SSRN Electronic Journal, 2019.

- Nyaradi J. Super Sectors: How to Outsmart the Market

Using Sector Rotation. Wiley, 2010.

- Yang YH, Pinsky E.

A simple rotation strategy

with sector etfs. Technical Analysis of Stocks and Commodities,

2022;40(12): 36-40.

- Joshi A, Deshmukh

PK, Lohokare J. Comparative analysis

of vanilla lstm and peephole lstm for stock market

price prediction. In 2022 International Conference on

Computing, Communication, Security and Intelligent Systems

(IC3SIS), 2022: 1-6.

- Moreno L, Alvarez M. Emerging market

adrs as portfolio diversifiers. Latin American Journal

of Finance, 2021.

- Assogbavi T, Osagie JE, Frieder LA, et al. Investment strategies, performance and trading information impact.

Investment Review, 2011.

- Block J, Maewal A. Deep sector rotation swing trading. SSRN Electronic Journal, 2023.