Enhancing Credit Risk Analysis in Financial CRMs using Retrieval-Augmented Generation and Predictive AI

Abstract

Credit risk evaluation has always been a

crucial part of the decision-making process in finance. However, researchers

face significant challenges trying to apply statistical models that are not

very malleable when it comes to reflecting the ever-changing behavior among

borrowers or the changes in the economic environment. A recent development in

machine learning, which can be categorized under Artificial Intelligence, is

the Retrieval-Augmented Generation (RAG). This paper proposes integrating RAG

with predictive AI models in credit risk analysis for financial CRM systems.

Thus, RAG systems enhance structured financial datasets since the derived

variables are real-time, borrower-specific and macroeconomic, enhancing the

accuracy and responsiveness of financial dataset predictions. Therefore, as

shown from the evaluations of the ChinaZJB SME dataset as well as other UCI

benchmark datasets, the integration of RAG improves the roots of traditional

prediction models, including Random Forest, Neural Networks, Support Vector

Machines and Logistic Regression in terms of accuracy, recall and AUC-ROC.

Further, the timely incorporation of new datasets reduces class imbalance and

enhances minor class prediction beyond 20%. It describes the system, which

includes the main elements, methods of data preparation, methods of training,

methods of building and selecting the model and data privacy issues. These

studies establish that integrating retrieval systems with AI shifts the

landscape of financial CRM technology to the next level of solutions that can

provide better customer experiences and agile and robust credit risk predictions.

The future development can be the progress in developing an efficient and

optimized retrieval system, integrating risk modelling for personal clients and

using the system in other financial decision-making.

Keywords:

Credit Risk Analysis, Retrieval-Augmented

Generation (RAG), Predictive AI, Financial CRM Systems, Machine Learning, Risk

Modeling.

1.

Introduction

Credit risk management has become a key

strategy that applies to the lending process to help manage and minimise the

probability of default on a loan to maintain financial stability. Consequently,

conventional risk measurement techniques primarily skewed toward historical

records and other financial ratios are inadequate in an unstable and globalized

world economy. With increasing competition, financial institutions are now more

focused on evaluating credit risk and for this purpose more effective and efficient,

accurate and interpretable models are also required1-3. Using dispensation, client data storage and

management, Fruit has developed from simple data storage and client database

retainers into comprehensive customer-contact response, portfolio monitoring

and decision-support tools. However, advanced credit risk analysis in CRMs has

been limited, especially due to inadequate scoring models and inflexible data

processing mechanisms. In order to tackle this deficit, there is a significant

potential for amending the existing financial CRMs by implementing innovative,

adaptive risk evaluation mechanisms that utilize voluminous real-time data

environments.

Retrieval-augmented generation (RAG) can

be considered the artificial intelligence breakthrough that incorporates large

language models with an information retrieval mechanism. By integrating such

data from outside the model, RAG offers a more up-to-date and broader base for

credit risk assessment. With the right AI models for borrower behavior,

macroeconomic signals and portfolio characteristics integrated to Risk risk-adjusted

growth, the effectiveness and dynamism of risk management in a financial CRM can

be elevated by RAG. This work unveils a new approach to combining

Retrieval-Augmented Generation and predictive methods into financial CRM

systems for intelligent credit risk analysis. The proposed architecture

simultaneously boosts the prediction performance, increases the

interpretability of the results and optimizes the computations. This paper

outlines the key aspects of the system design, such as data source

identification, data retrieval approach, model incorporation and system

efficiency assessment. Concerning research findings attained from real-world

financial datasets, the presented approach can outcompete previous risk models,

permitting financial organizations to yield more accurate, quicker and more

reliable credit decisions within a rising-native financial world.

2.

Related Work

2.1. Traditional credit risk models

Traditional credit risk models have been organizations’

primary framework in evaluating default risk, loss frequencies and regulatory

capital charges. Models like Credit Metrics™ used by J.P. Morgan or Credit Risk

+™ of Credit Suisse companies follow the default mode or the mark-to-market

approach to determine the behavior of credit portfolios. Such systems primarily

refer to historical data for borrowers, internal credit scores and non-changing

financial ratios for risk measurement. A characteristic that most of these model’s

share is that they are unconscious models of credit risk where comparisons

between borrowers’ characteristics and their defaults are relatively static or

invariant to credit cycles4-7. However,

it becomes ineffective, especially in complex or changing economic scenarios of

the Italian economy, which are dynamic. They cannot take and respond to

real-time cues that the economy provides, for instance, changes in interest

rates, geopolitical risk or a particular sector’s decline. Reliance on past

information limits them in evaluating non-conventional borrowers or fresh

financial risks. Especially in economic distress, these constraints will result

in under or overestimating risks, portfolio vulnerability and regulatory compliance.

2.2. Use of AI and machine learning in

risk assessment

AI and ML have revolutionized credit risk

analysis by improving ways to inspect data and find unknown relations within

big data space. Tools like Random Forest, Support Vector Machines (SVMs) and

different types of Neural Networks also help risk analysts to integrate all

sorts of structured & unstructured hard & soft data records like

Transaction history, Geo mapping data and Behavioral Patterns from Social media

posts. Random Forests are much more likely to detect more complex borrower risk

factors than a single decision tree. Deep Neural Networks are very proficient in

modelling complex variable interactions. However, the implementation of these

models has been subject to criticism due to the interpretability of the models.

AI algorithms operate based on unexplained models, making it challenging for

financial institutions to explain credit decisions to regulators and auditors.

To this end, methods such as Shapley values and LIME (Local Interpretable

Model-Agnostic Explanations) have been created to provide much more

interpretability without much reduction in accuracy. Nevertheless, critics of

Artificial Intelligence have raised issues of data privacy, bias and fairness

in the model; however, they have proven their competence in bringing down

default rates, improving credit scoring and credit risk assessment, as well as

extending credit accessibility to under-banked and unbanked populations hence

revolutionizing the risk assessment market.

2.3. Retrieval-augmented generation (RAG)

in financial applications

Retrieval-augmented generation (RAG) is a

crucial development, particularly FOR artificial intelligence applications

entailing action-based creativity, which dynamically correlates with existing

information. RAG architectures enable models to retrieve the latest information

from databases and/or the web to provide accurate and timely information in

responses to queries processed. The large language models (LLMs) introduced

into the RAG architectures provide an ability to bring external data for the

current and accurate output. In a credit risk analysis, RAG allows an organization’s

CRM systems to integrate up-to-the-minute financial conditions, changes in

regulations and borrower information into its risk assessment processes. For

instance, when using a RAG-enhanced CRM, the ability to obtain up-to-date

macroeconomic factors such as unemployment rates, inflation rates or policy

shifts together with borrower-specific changes such as revised income or

spending are used to fine-tune the risk measurements even further. This

addresses the knowledge cutoff major drawback that has been realized in most AI

models and also ensures that there are minimal hallucinations because the

answer is obtained from an authoritative source. Automated compliance

reporting, anti-money laundering (AML) screening and personalized investment

advisory are also some of the applications many financial institutions use RAG

for, apart from credit scoring. Since RAG offers tangible and transparent

results supported by proof, the system is a pioneering tool in the

metamorphosis of smart, compliance-conscious and adaptive financial CRM

solutions.

3.

Proposed Methodology

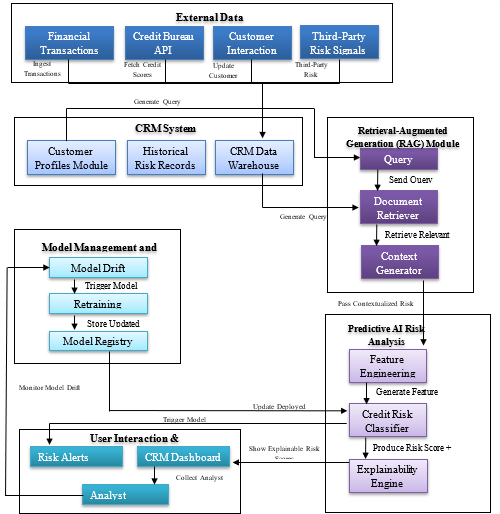

3.1. System architecture overview

The architecture of the proposed approach

that enriches credit risk analysis in financial CRM systems comprises real-time

data ingestion, Retrieval-Augmented Generation (RAG) for dynamic contextual

retrieval and advanced Predictive AI models for risk classification. The

overall system is presented in Figure 1 below and is designed to prevent such

drawbacks of a static model by regularly incorporating external financial

indicators and customer behavior signals into the risk assessment8-12. This can be achieved by designing the

application modularly, where data flows from external sources, through

individual CRM system components, into RAGs and then to the predictive analytic

engines. At the base, the system takes multiple raw, non-structured inputs in

financial transactions, raw credit bureau feeds, communication records and

other external signals, such as market updates or fraud trends. Over time, it

is kept in the CRM Data Warehouse with in-house information such as customer

database risk evaluation. The results of each query are query embeddings that

express a certain risk profile of the customer, which allows for information

search and retrieval by the RAG module within a particular context.

The Retrieval-Augmented Generation (RAG)

is designed to act as the final link between static CRM data and real external

knowledge. As an information search technology, it processes analyst queries,

searches for relevant documents and provides rich contextual data. This output

is then entered into the Predictive AI Risk Analysis engine, which means that

credit risk scores are not only based on static attributes of a borrower but,

in addition to that, are supplied with real financial and behavioral data. For feature

engineering, risk scoring and feature explanation, the predictive engine uses a

combination of XG Boost, deep neural nets (DNN) and decision trees. In order to

ensure that the assembling remains stable and the model remains relevant to the

selected system, there is the Model Management and Feedback Loop responsible

for evaluating the performance and checking for model shifts. Whenever there is

a change in dataset characteristics or model performance, the regulation of

retraining processes, update of the deployed models and registration happens

systematically. Records are updated constantly in an interactive CRM dashboard,

which enables the risk taker to either ratify or dispute the risk scores

assigned by the application, thus eliminating the human-in-the-loop dilemma.

Last, the User Interaction and Monitoring

module includes the real-time risk profile visualization, the risk score

rationale and the heat-map interface. The analysts can look at specific

customer data tables with selected fields, work with new risk alerts to follow

and provide feedback that improves the algorithms used in the models (Figure

1). This synergy makes it possible to improve the accuracy and timeliness

of credit risk analysis while simultaneously making it more transparent and

easier to audit in a world that is ever more concerned with the explainability

and fairness of the actions undertaken using Artificial Intelligence.

Figure 1: System Architecture for Enhancing Credit Risk Analysis in Financial CRMs using RAG and Predictive AI.

3.2. Data sources and preprocessing for CRM

systems

The modern approach to credit risk

analysis in connection with the use of modern CRM systems involves using many

various but high-quality sources of information. The proposed framework

receives data from conventional finance sources and new advanced sources. The

external data include the financial transaction databases, credit bureau APIs,

customers’ interaction logs and third-party risk signals. Each provides value

for real-world spending patterning, scoring normalized for risk benchmarking

and customers’ raw interacting patterns and sentiment. However, preprocessing

is always required before the datasets can be used in analytical models. Data

preprocessing techniques are practiced to deal with problems related to missing

data, inconsistent data format and errors in entries. Normalization and feature

scaling normalize or scale the numbers involved in order to bring all

attributes from different sources to the same order. Thus, for the case of

unstructured data like customer logs/risk alerts, features are derived from

them using natural language processing (NLP). Furthermore, the entity

resolution methods help to connect the customer data from various sources and

enrich the consolidated customer view in the CRM Data Warehouse. This is very

important to enhance the quality of the data to allow subsequent processes,

such as the RAG module and the Predictive AI Engines, to run without

interruption.

3.3. Retrieval-augmented generation (RAG)

for contextual credit analysis

The RAG module is critical in changing the

CRM data from passive to active and contextual credit risk information. In

contrast to other dialogue modular systems, RAG does not contain pre-stored

information required for the credit assessment. Still, it dynamically builds

its context from real-time documents important for the current assessment task.

When the Query Encoder component receives a query that can be consistent or

created by the risk analyst based on some observed situation, the component

takes the representation of an analyst’s query and the context of the customer.

This vector is then given to the Document Retriever, which retrieves the

updated risk documents relevant to the identified sources from both internal

and external sources that have been indexed. The documents are then compiled

into information packages by the Context Generator, including recent trends in

finance behavior, regulation changes and the macroeconomic environment. In this

way, RAG excludes the impact of such key issues as high dependence on outdated

information and high probabilities of appearing hallucinations, which are

inherent to the work of traditional language models. This real-time

contextualization makes it easier to get updates about the borrower's current

risk environment, making credit risk scores timelier and more accurate for

financial decision-making.

3.4. Predictive AI models for risk scoring

The Predictive AI Risk Analysis engine

performs the classic quantitative risk rating if the input is contextualized. In

order to start with, there exists the Feature Engineering Engine that works by

converting the big contextual data into vectors suitable for the efficiency of

machine learning models. The interactions of features, which include feature

crossing and embedding layers as well as the use of feature extraction tools

such as principal component analysis (PCA). The core classifier is an ensemble

of XG Boost, deep neural networks (DNNs) and decision trees for improved

accuracy and stability of the model. After the credit risk score has been

computed, the Explainability Engine adds brief explanations to its output for

human understanding. The explanations on risk assessment are based on methods

such as Shapley value decomposition and attention heatmaps that focus on the

important features and events that led to the final decision. It also assures

compliance with the legal aspects, thus increasing the level of trust between

the lenders and borrowers and, at the same time enables the analyst to arrive

at quicker decisions about the loans to offer. The proposed model architecture

of the hybrid allows the avoidance of overfitting, the ability to detect new

risk patterns and integration with continuous learning.

3.5. Integration strategy into financial CRMs

Seamless integration into existing

financial CRM systems is critical for maximizing the utility of the proposed

framework. This way, the architecture is designed for modular deployment where

Financial Institutions can implement the framework and components in stages

depending on their technological advancement and business needs. The main role

of the CRM Data Warehouse is to provide mediation and integration, receive data

from the external data ingestion layers and the RAG module and work with the

predictive analytics engine and users’ dashboards through APIs only. These are

procedures such as encryption, access control and logging to ensure that customer’s

information is secured throughout the data flow process. In order to provide a

good user experience, the Risk Alerts Module and the UI for the CRM Dashboard

contain alerts, clickable heat maps and search functions to help the user find

a specific customer. Notably, the Analyst Feedback Collector is a part of the

CRM, which helps update the model, achieving the human-in-the-loop model and

improving the level of risk scores. Using the Model Management and Feedback

Loop means that models are updated as often as needed based on market changes.

Using xAI means that outcomes obey the Fair Credit Reporting Act (FCRA) and

Basel III benchmarks. Therefore, the integration aims to enhance incumbent CRM

solutions whilst avoiding service interruption to facilitate the building of a

smarter, more flexible and less vulnerable credit risk management framework.

4.

Implementation Details

4.1. Technology stack and tools used

The technologies used in implementing the

proposed credit risk analysis system are based on the technological stack that

will allow for scalability and performance of the analysis, as well as how

easily the technology can be integrated with the overall system13-16. For data storing and processing,

cloud relational databases like Amazon RDS and Azure SQL are used and data

repositories such as Amazon S3 are used for dealing with the large amount of

semi-structured transaction logs and interaction data. Data preprocessing is

conducted in Python with the help of Pandas, NumPy and spaCy for manipulating

both structured and unstructured data. The Retrieval-Augmented Generation (RAG)

module is developed using Hugging Face’s Transformers and FAISS (Facebook AI

Similarity Search) to index documents and passages. For the predictive AI

models, suitable frameworks like XG Boost, TensorFlow, Py Torch, et cetera are

used to develop and deploy the machine learning models to handle high

dimensional feature space. The tools used for developing the interactive CRM

interface and dashboards include React.js, While the CRM platforms used are

force.com (Salesforce) and Microsoft dynamics via RESTful APIs. Kubernetes is

used to manage the containers of the services to easily deploy and scale them,

while tools such as ML flow are used to track the models throughout the

development process (Table 1).

Table 1:

Technology Stack Used for Enhancing Credit Risk Analysis in Financial CRMs

|

Component |

Technology/Tool |

Purpose |

|

Data Ingestion |

Apache

Kafka, ETL Scripts |

Real-time

data streaming & transformation |

|

Preprocessing |

Pandas,

NLTK, spaCy |

Cleaning

structured/unstructured data |

|

Retrieval Layer |

ElasticSearch,

FAISS |

Fast

document/vector retrieval |

|

Language Model |

OpenAI

GPT / BERT / T5 |

Text

generation and embedding |

|

ML Framework |

PyTorch,

TensorFlow |

Model

training and deployment |

|

Visualization |

Plotly,

Tableau |

Interactive

dashboards |

|

Compliance Tools |

SHAP,

LIME, Differential Privacy |

Model

explainability and data protection |

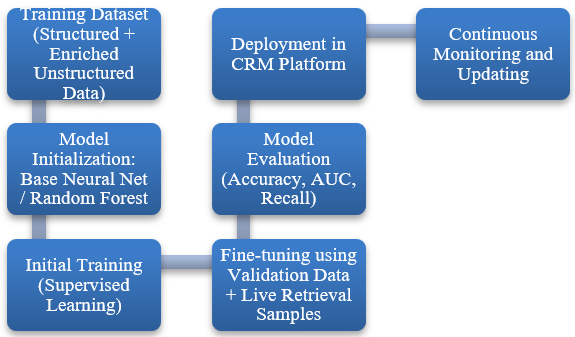

4.2. Model training and fine-tuning

processes

The processes of model training and model

fine-tuning are extremely important in order to enhance the ability of the

system to predict accurately as well as to be robust over the long run. First,

the baseline models are trained on historical credit performance data in which

default, delinquencies, repayment history and other aspects are labelled. Thus,

for the Retrieval-Augmented Generation module, large language models are

trained on the financial and credit report, regulatory bulletins and credit

analyst notes to attune the model to process financial jargon and focus on that

particular type of language. Fine-tuning, on the other hand, works under

transfer learning methods where the transformer models are trained on some

other specific datasets with small learning rates during training to avoid the

issue of catastrophic forgetting. Techniques such as grid search and Bayesian

optimization are used to finalize model structures so that the chosen

performance measures undergo optimization: AUC-ROC and the balance between

precision and recall.

Furthermore, to cater for the problem of model drift that arises during the deployment process, a continuous training process is set up. This pipeline takes newly acquired risk events and feedback from the analysts to improve and update the models in the pipeline without needing to retrain the model from scratch. This technique enhances adaptability without interrupting operations.

Figure 2: AI Model Training and Fine-tuning Workflow.

4.3. Handling data privacy and compliance

Given the sensitive nature of financial

and customer data, robust strategies for handling data privacy and compliance

are integral to the system’s architecture. Customer-identifiable information

(CII) is also preserved through the Secure Sockets Layer or Transport Layer

Security protocol at both storage and transit with the use of protection

schemes like Advanced Encryption Standard ciphering or AES-256 and Transport

Layer Security stand TLS 1.3. RBAC is implemented at different levels within

the system whereby only authorized people are allowed access or make changes to

the sensitive data17-20. As data

is removed in tasks where possible, data anonymization and tokenization are

applied where there is a need to replace specific data during the training

phases. In order to ensure GDPR, CCPA and FCRA compliance, settings of audit

trails and consents are automated. Audits of data access and penetration

testing, as well as employing the services of third-party security assessors,

are performed to reduce these risks ahead of time. The robust explainability

architectures developed into the appropriately selected AI solutions can also

support the reporting requirements to the regulators and enable reporting for

the ruling for adverse consumer credit decisions.

5.

Experimental Setup and Results

This section describes the experimental

setting that will be employed to assess the performance of Retrieval-Augmented

Generation (RAG) in credit risk analysis against traditional machine learning

methods. It is detailed in the experiments that predictive performances,

insensitivity to imbalanced classes and abilities for dynamic updating of

models based on borrower information have been considered.

5.1. Dataset description

In order to enhance the validity of the

study, this research employed two major data sets, The ChinaZJB SME dataset and

several credit datasets from UCI. The ChinaZJB SME dataset stems from the

annual loan ledger of a Chinese commercial bank and features the information of

1,329 SMEs, out of which 108 are defaulting and 1,221 are non-defaulting. The traditional

analysis involves reports on financial ratios, additional loan details, credit

rating and non-financial parameters. First of all, serious problems of class

imbalance are notable as, on average, there is one default for 11 non-defaults.

For assessing robustness across different environments, the work used UCI

benchmark datasets. These comprise the Polish bankruptcy data (versions 1 to

3), the Australian credit approval data and the Taiwan credit card default data

(Table 2).

Table 2:

Summary of Datasets Used for Model Evaluation.

|

Dataset |

Samples |

Defaults |

Non-Defaults |

Imbalance

Ratio |

|

ChinaZJB

(SMEs) |

1,329 |

108 |

1,221 |

1:11 |

|

UCI Polish 1 |

7,026 |

275 |

6,751 |

1:25 |

|

UCI

Australian |

690 |

307 |

383 |

1:1.25 |

5.2. Evaluation metrics

In order to provide a holistic assessment

of model performance, multiple evaluation metrics were utilized. Accuracy

determined the number of correct classifications concerning the total number of

cases. At the same time, precision assessed the capability of minimizing false

positives by looking at the number of true positives against the total

predictions made. Regarding recall, the emphasis was on the ability to detect a

reasonable number of defaulters; it involved determining the percentage of

actual defaulters that were accurately captured. The F1 Score, a combination of

precision and recall indicators, was particularly used to analyze the results

for markers for the imbalanced datasets. The AUC-ROC model was used to check

the model's capacity in classifying between a defaulter and a non-defaulter

using different threshold levels.

5.3. Baseline comparisons

The following compares the traditional

machine learning models and the developed RAG-enhanced credit risk system. For

training information only that was in structured data format, we had Random

Forests, Neural Networks, Support Vector Machines (SVMs) and Logistic

Regression models (Figure 3). At the same time, RAG systems used the

data in structure formats plus dynamic data from unstructured databases (Table

3).

Table 3:

Performance Comparison of Traditional Machine Learning Models.

|

Model |

Accuracy |

AUC-ROC |

Precision |

Recall |

F1

Score |

|

Random Forest |

93% |

0.94 |

0.91 |

0.88 |

0.90 |

|

Neural

Networks |

91% |

0.92 |

0.89 |

0.86 |

0.87 |

|

Support

Vector Machine (SVM) |

89% |

0.88 |

0.82 |

0.84 |

0.83 |

|

Logistic

Regression |

84% |

0.79 |

0.78 |

0.76 |

0.77 |

Figure 3:

Graphical Representation of Performance Comparison of Traditional Machine

Learning Models.

5.4. Performance analysis of RAG vs traditional

models

The introduction of Retrieval-Augmented

Generation into the credit risk assessment pipeline yielded substantial

improvements across all major evaluation metrics. Concerning the ChinaZJB SME

classification task, the RAG-enhanced systems could provide results of around

95 % accuracy, which was much higher than the baseline Random Forest. This

improvement mainly came from behavioral data of borrowers, transaction

stability and sentiments from social media, which gave a real-time indication

of the health of the borrowers.

RAG models achieved a better AUC-ROC of

0.96 than the Random Forests, with an AUC-ROC of 0.94 only. Indeed, this level

of discriminative power is explained by the capacity of RAG to integrate

real-time macroeconomic factors (such as employment statistics or

sector-specific information) when it is evaluated. Further, RAG systems kept a

precision of 0.93 and a recall of 0.90. Thus, false positives were very low

while the right clients at risk were identified. Significantly, RAG was able to

claim that their capacity to process external big data contributed greatly to

the issue of class imbalance. These rates show the effectiveness of

RAG-enhanced systems in contrast with the previous models and these had an

increase of approximately 22% of the minority class (default prediction), which

can help in the early identification of high-risk customers. Thus, enhancing

the adaptive context-awareness of credit risk prediction requires the integration

of the retrieval mechanisms with the machine learning model for more efficient

credit risk prediction.

6.

Discussion

The corresponding analysis of the results

obtained from the experiment showed that using the Retrieval-Augmented

Generation (RAG) in financial CRM systems significantly improves credit risk

assessment. RAG makes models have situational awareness, as they can update

their behavioral data of a specific borrower and macroeconomic indicators in

real-time, which is not characteristic of traditional AI. This real-time

contextualization also enhances the marksmanship and recall, as well as the

identification of early warning signs of borrower’s behavior, which will help

to promote the effectiveness of risk management. Especially for imbalanced data

sets where defaults are few but important for detection, like our ChinaZJB, the

RAG-augmented models have been found to have 22% higher Minority Class Recall,

which can revolutionize how institutions could contain credit risk.

RAG-enhanced systems lead to enhanced

performance levels; however, it brings new challenges. Managing external data

acquisition in real-time processing truly calls for a well-organized,

well-equipped framework, better and stringent validation and verification

principles and considerable and sophisticated query optimization measures to

achieve both reliability and control of latency. However, privacy, compliance

(i.g.., GDPR, CCPA) and ethical usage of unstructured data will always be

critical for maintaining regulators’ approval and clients’ trust.

Interpretability mechanisms such as explainability engines are even more

important when the model’s features or predictions depend on information that

can change in a short time, like social media updates. Financial institutions,

hence, have to consider the two elements of superior and optimum prediction as

they also foster openness, responsibility and regulation of artificial

intelligence-based decisions. Transitioning from RAG into predictive credit

risk analysis is a great leap towards the next generation of financial CRM

systems. This not only helps firms predict defaults more accurately but also

makes them improve constantly in adjusting to the economic conditions that

constantly change. Future work in this regard might consider a refinement of

the retrieval approach, the application of reinforcement learning for better

risk management and the use of federated learning for improved data privacy

during the usage of downstream external data sources.

7.

Future Work

The future advancements in the retrieval

systems will enhance the efficiency, precision and relevance of the information

retrieved during credit risk assessments. Many current approaches based on RAG

models have issues such as high retrieval latency and noise when it comes to

unstructured information. This can be achieved with the help of using such

techniques as dense passage retrieval, knowledge graphs and multi-hop retrieval

chains of the sources. Moreover, the inclusion of some kind of reinforcement

learning-based feedback option can be introduced that would help make the

learning process in the given retrieval systems dynamic by revealing which

sources are most trustworthy and therefore more contextually relevant and

helpful, for different types of borrowers by improving the precision and speed

of risk predictions.

Personalized credit risk modelling is

another area of growth in the field in the future. Standard credit scoring

procedures provide little distinction between borrowers in the same risk

profile or age. However, the next-generation systems are ideally positioned to

create even truly accurate risk scores using RAG combined with much more

detailed borrower characterization targeting not only transactional behavior,

real-time social media phenomena and even borrowers’ economics. It would

facilitate accurate differentiation of credit products, customized setting of

the interest rate structures and the ability to monitor early warning signs of

firms in distress for each customer, thus enhancing customer satisfaction and

portfolio performance. However, the general idea of applying RAG and predictive

AI in other aspects of financial decisions goes further than credit risk

analysis. Some applications include investment advisory services, anti-money

laundering (AML) tools, insurance and claims underwriting, particularly when it

involves real-time retrieval. The following are some examples: active

management of investment portfolios based on real-time data on geopolitics

events and the use of the Internet to adjust insurance premiums based on

lifestyle data. It is believed that as information retrieval systems continue

to grow in terms of their capabilities in terms of scalability and context

sensitivity, there will be significant growth in the use of these systems

within the financial sphere to make more responsive or more data-driven

decisions.

8.

Conclusion

This study demonstrates the transformative

potential of integrating Retrieval-Augmented Generation (RAG) with predictive

AI models in the context of credit risk analysis for financial CRM systems. By

Incorporating RAG, methods improve the modelling precision and recall and

reduce sensitivity to class imbalance about more conventional machine learning

solutions achieved by combining structured financial data and real-time

external data retrieval. Hence, RAG’s capability of responding to borrower behaviors

and macroeconomic changes makes it a critical tool in applying agile and smart

credit risk management strategies.

RAG also incompletely solves important

problems of descriptive AI, such as the knowledge cutoff problem and static

risk profiling. Applying current values of the market changes in regulations

and evaluating the borrowers ‘behavior signals lets the financial institutions

adapt quickly to economic conditions. However, to adopt and implement RAG

systems, revision of data governance, model explainability and regulating

requirements are necessary to enhance trust. In conclusion, this paper presents

RAG-enhanced predictive AI as a symbolic direction toward improving the

financial decision system. Future research development will also focus on improving

the retrieval technique, communicating risk assessment and bringing horizons to

other segments of the financial industry. That way, such changes can make a

difference for financial institutions to deliver higher accuracy, fairness and

efficiency in risk assessment and client engagement.

9.

References

- Wang

Z. Artificial Intelligence and Machine Learning in Credit Risk Assessment:

Enhancing Accuracy and Ensuring Fairness. Open Journal of Social Sciences, 2024;12:

19-34.

- Giudici

P, Hadji-Misheva B, Spelta A. Network-based credit risk models. Quality

Engineering, 2020;32: 199-211.

- Mays

E. Credit risk modelling: design and application. Global Professional Publishing,

1998.

- Aziz

S, Dowling M. Machine learning and AI for risk management. Springer

International Publishing, 2019: 33-50.

- Pedron CD, Picoto WN,

Dhillon G, et al. Value-focused objectives for CRM system adoption. Industrial

Management & Data Systems, 2016;116: 526-545.

- Paltrinieri

N, Comfort L, Reniers G. Learning about risk: Machine learning for risk

assessment. Safety Science 2019;118: 475-486.

- Hegde

J, Rokseth B. Applications of machine learning methods for engineering risk

assessment- A review. Safety Science, 2020;122: 104492.

- Sharma

A, Singh UK. Modelling of smart risk assessment approach for cloud computing

environment using AI & supervised machine learning algorithms. Global

Transitions Proceedings, 2022;3: 243-250.

- Zhang

B, Yang H, Zhou T, Ali Babar M, Liu XY. Enhancing financial sentiment analysis

via retrieval augmented large language models, in Proceedings of the fourth ACM

international conference on AI in finance, 2023: 349-356.

- Pan J, Yang Q, Yang Y, et al.

Cost-sensitive-data preprocessing for mining customer relationship management

databases. IEEE Intelligent Systems 2007;22: 46-51.

- Peppard

J. Customer relationship management (CRM) in financial services. European Management

Journal 2000;18: 312-327.

- Siddiqi

N. Intelligent credit scoring: Building and implementing better credit risk

scorecards. John Wiley & Sons, 2017.

- Ryals

L, Payne A. Customer relationship management in financial services: towards

information-enabled relationship marketing. Journal of strategic marketing, 2001;9:

3-27.

- Zheng

H, Shen L, Tang A, et al. Learn from model beyond fine-tuning: A survey, 2023.

- Kamath

CN, Bukhari SS, Dengel A. Comparative study between traditional machine

learning and deep learning approaches for text classification. In Proceedings

of the ACM Symposium on Document Engineering, 2018: 1-11.

- Chauhan

NK, Singh K. A review of conventional machine learning vs deep learning. In

2018 International Conference on Computing, power and communication

technologies (GUCON), 2018: 347-352.

- Delamaire

L. Implementing a credit risk management system based on innovative scoring

techniques (Doctoral dissertation, University of Birmingham), 2012.

- Siddiqi

N. Credit risk scorecards: developing and implementing intelligent credit

scoring. John Wiley & Sons, 2012;3.

- Wu TC, Hsu MF. Credit risk

assessment and decision-making by a fusion approach. Knowledge-Based Systems, 2012;35:

102-110.

- Doumpos M, Lemonakis C, Niklis D, et al. Analytical techniques in the assessment of credit risk. EURO advanced tutorials on operational research, 2019.