FDIC Resolution & Regulatory Submissions: Traceable, Reconciled Data Pipelines for Large Financial Institutions

Abstract

Resolution planning and high-frequency regulatory submissions have

become critical supervisory expectations for systemically important financial

institutions. Regulators such as the Federal Deposit Insurance Corporation

(FDIC) increasingly require institutions to demonstrate not only accuracy and

timeliness, but also traceability, reconciliation and audit-ready lineage

across complex enterprise data environments. Traditional regulatory reporting

architectures-often fragmented, manual and opaque-are insufficient to meet

these expectations, leading to reconciliation breaks, delayed submissions and

extensive regulator follow-up queries. This paper presents a reconciled,

traceable data pipeline architecture designed to support FDIC resolution

planning and recurring regulatory submissions for large financial institutions.

The proposed framework integrates controlled reference data, dual-control

reconciliations, deterministic aggregation logic and reproducible reporting

outputs. Emphasis is placed on end-to-end lineage, from source systems through

transformation layers to regulatory schedules, enabling transparent

auditability and rapid regulator Q&A response. The methodology incorporates

standardized ingestion patterns, metadata-driven transformations, reconciliation

checkpoints at each processing stage and a rigorous testing matrix spanning

unit, integration, regression and scenario testing. A governance-aligned

control framework ensures segregation of duties, change management discipline

and submission certification accountability. Results from an enterprise-scale

implementation demonstrate measurable improvements, including reduced manual

adjustments, accelerated submission timelines, improved data quality metrics

and enhanced regulator confidence. The findings indicate that reconciled

pipelines are foundational to sustainable compliance, particularly under

increasing submission frequency and supervisory scrutiny. This paper

contributes a practical, scalable model for regulatory data engineering in the

context of FDIC resolution requirements.

Keywords: FDIC resolution planning, Regulatory reporting, Data

lineage, Reconciliation controls, Audit-ready pipelines, Financial data

governance

1. Introduction

1.1. Background

Following the world

financial crisis, the regulatory authorities the world over came up with

heightened resolution planning criteria to reduce the systemic risk posed by

large and complex financial institutions1,2.

The Federal Deposit Insurance Corporation (FDIC) in the United States requires

the resolution plans (also known as living wills), to be submitted that show

how a firm might be resolved in an orderly fashion without assistance by the

taxpayers. Originally developed as more or less fixed documents, these plans

have turned into very data-intensive and recurring regulatory filings that

require regular operational discipline. These submissions have highly increased

their range to incorporate granular balance sheet breakdowns, liquidity

measures and legal entity exposures, derivatives stands and additional vital

financial and risk information. To satisfy these needs, it is important to have

regular and reconciled flows of data in many domains, such as finance, risk,

treasury and operational systems, each of which could have its own data

structures and reporting conventions. Regulators have become more attention

able to the fact that compliance is not only a question of the number of

figures on the balance sheet but they also need to have transparent, traceable

and reproducible reporting frameworks. This implies that the reported

aggregates should be supportable, have an evident audit trail of how the data

copy came to the aggregation system through transformation and submission. This

in practice necessitates a complete data governance, centralized reference data

management, deterministic transformation and aggregation logic and sound

reconciliation processes. The regulatory emphasis on traceability and

reproducibility is an expression of a wider supervisory aim, namely to make

sure that firms can adequately demonstrate operational resilience and provide

timely and reliable information under normal and extreme circumstances so as to

enhance the stability of the financial system overall.

1.2. Needs of FDIC resolution &

regulatory submissions

The large financial institutions are highly demanded in terms of operational accuracy and governance structures by the FDIC resolution planning and the regulatory submissions that accompany the planning process3,4. The needs can be classified in several major areas (Figure 1):

Figure 1: Needs of FDIC

Resolution & Regulatory Submissions.

- Comprehensive data integration: Resolution plans

need data of different functional area to be aggregated such as finance, risk,

treasury and operations. Multiple sources with different schemas, data

standards and frequencies of updates, which consist of different institutions,

need to be combined in a unique reporting pipeline. This integration helps to

assure that all the regulatory submission is consistent, complete and aligned

with the statutory financial and risk exposures of the institution.

- Data accuracy and reconciliation: In order to have the

confidence of the regulators, precise and reconciled data is essential. The

FDIC and other oversight regulators anticipate that the reported figures,

including balance sheet decompositions, liquidity positioning as well as legal

entity exposures, be aligned not only within individual systems but also

between and among systems. Aggregated data integrity requires multi-dimensional

reconciliations, which encompass legal entities, product lines, currencies and

exposures to counterparty to prompt inconsistencies capable of attracting

regulatory enquiries.

- Traceability and lineage: The regulators are

placing more importance on traceability and explainability of the reported

data. All the figures supplied in a resolution plan should be identifiable to

source systems, documented transformations, aggregation rules and reference

data mappings. Such a degree of data lineage can guarantee submissions can be

reproduced, can be reviewed by an audit or other supervisors and makes all

reported metrics more defensible at a glance.

- Operational controls and governance: It also needs

powerful governance structures to contain the confusion and danger of repeated

submissions. The key requirements that institutions should introduce are the

controlled reference data hubs, approval workflows, version control and

effective-dated change management. Concerted balances, regularized verification

process, on-format testing cycle are needed in order to ensure consistency,

less manual intervention and measurement of the operational risk.

- Timeliness and regulatory compliance: The submission of

high-frequency regulatory submissions requires timelines. The institutions

should have in place procedures that enable points of data freeze, sign-offs of

reconciliation, management certification and submission in a timely manner. It

is imperative to meet these deadlines and be able to achieve the accuracy and

completeness of the data so as to be able to retain regulatory trust and show

preparedness to operate under the possible resolution scenarios. Taken together

these requirements point to the fact that FDIC resolutions and regulatory

submissions cannot be viewed as mere reporting activities, but in order to

facilitate transparency, reproducibility and quick regulatory reaction a

well-developed, integrated and auditable data infrastructure is necessary.

1.3. Regulatory submissions: Traceable, reconciled

data pipelines for large financial institutions

Regulatory

submissions in relation to large financial institutions have become extremely

complicated activities, which demand more than mere data reporting5,6. More and more certainly, regulators like

the FDIC and other supervisory agencies are demanding not only numerical

accuracy but also traceability in all reported metrics in addition to

reproducibility and reconciliation. This has brought about a need to come up

with traceable, reconciled data pipelines that could combine information across

diverse functional areas such as finance, risk, treasury and operations. These

pipelines are the foundation of regulatory reporting in which institutions are

able to generate quality and defendable data, both with consistency and

efficiency. Traceable data pipes are end to end, meaning that each figure that

is reported can be tracked to the underlying systems, transformations and

aggregation logic. It involves comprehensive lineage of transactional data,

reference data and calculation procedures so that regulators need not have to

question reported measures since they can self-test and recreate them.

Traceability minimizes chances of errors, enhances auditability and enables

quick response to supervisory questions especially in the context of resolution

planning where real time and correct reporting is crucial. The reconciliation

in the given pipelines is complementary since it ensures the data survey

evenness among various aspects including legal entities, product lines,

currencies and counterparty IEs. Multi-layered, automated reconciliations

(source-to-ingestion, ingestion-to-transformation and aggregation-to-output)

are effective to identify discrepancies at an early stage as well as avoiding

the spread of errors. This will reduce the state of man-hands, operational risk

and expediture and the submission cycles, making institutions able to meet the

arm-twisting regulation time frames without quality of data being compromised. Also,

the strong governance and control systems, such as centralized reference data

control, aggregation logic versions and formal approval processes, strengthen

the pipeline integrity. Through the integration of traceability, reconciliation

and controls into the architecture, the financial institutions, which are

large, can make sure that the regulatory submissions made by them are not

solely accurate but they are also auditable, repeatable and in line with the

changing supervisory expectations. Such pipelines can be used to ensure that

regulatory reporting is resilient and proactive rather than reactive and the report includes both compliance and

operational efficiency.

2. Literature Survey

2.1. Regulatory reporting architectures

The regulatory

reporting environment has changed dramatically and the sphere of

report-oriented and siloed process to support and interpret data-driven

architectures7-9. Principles

supporting effective risk data aggregation and risk reporting (BCBS 239) by the

Basel Committee on Banking Supervision are foundational directions that state

essential requirements in regards to the accuracy, completeness, timeliness and

flexibilities of the data. These doctrines have had a potent power in shaping

patterns of thinking in supervisory and industry designs. These requirements

are however extensively addressed in the literature at a conception level which

has little to say on how companies can practically implement them in complex

legacy systems. White papers on industry and publications by vendors often

recommend centralized regulatory data lakes or enterprise reporting systems,

whereas in fact the reconciliation, control and governance provisions on which

such resolution planning and supervisory scrutiny will depend.

2.2. Data lineage and auditability

Data lineage and

auditability Studies on data lineage and auditability are mainly concerned with

metadata management, provenance tracing and technical traceability of data

pipelines. In financial services, though, lineage has an extra regulatory

aspect: financial institutions are expected to be able to justify, defend and

recreate any given reported figure of business and regulatory substance.

Supervisory expectations are larger than system-to-system traceability with

clarity of data ownership, logic of transformation and compliance to required

regulatory definitions. Current lineage models often focus on the technical

processes at the expense of resolving the gap between the raw data, business

semantics and regulatory interpretation, making them ineffective with

regulatory reporting and examination needs.

2.3. Reconciliation frameworks

Literature on

reconciliation also focuses on the fact that it is the financial control

processes that include the reconciliation of sub-ledger balances against the

general ledger to enhance accounting integrity. These strategies are quite

established in the reporting of financials, but they are not adequate in terms

of regulatory resolutions filings, which must be reconciled on various levels,

including legal entities, product, currency and counterparty hierarchies. The

resolution-related data also should be in a position to reconcile with risk,

finance and treasury areas and this is usually on a tight time schedule. The

literature does not have sufficient advice on how to expand the reconciliation

frameworks past accounting constructs in order to facilitate regulatory

submissions where heterogeneous data source and supervisory viewpoints are

aggregated.

2.4. Gaps identified

A weakness in the

literature on regulatory architecture, data lineage and data reconciliation, is

the lack of a holistic, end-to-end framework, integrating governance, controls,

lineage, reconciliation, plus testing into a single reporting pipeline on

regulations. The current research and industry trends would look at these factors

singly, thus coming up with piecemeal solutions that can never pass the

scrutiny of the supervisor. It is interesting to note that scholarly or

practitioner literature is scarce that describes operationally proven

architectures that are explicitly aligned with expectation of resolution

authority, e.g., the expectations of the FDIC. The paper aims to fill this gap

with a set of proposed, unified, regulator-friendly architecture that is based

on reality experience in implementation.

3. Methodology

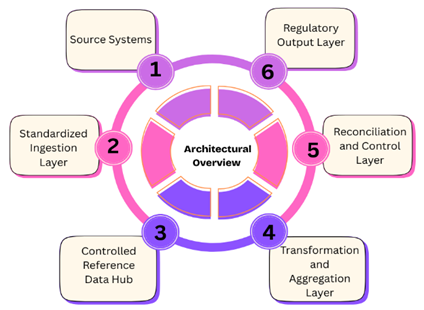

3.1. Architectural overview

The proposed

regulatory reporting pipeline will be developed as a layered architecture,

which will enhance regulatory traceability, control and modularity10-12. The levels have their own functions as

well as help in end-to-end data lineage, reconciliation and governance. This

isolation of concerns makes it scalable, review of by supervisors is made easy

and it makes it possible to have an individual part of the reporting process

evolve without jeopardizing the integrity of the entire process (Figure 2).

Figure 2: Architectural

Overview.

- Source systems: At the heart of the

architecture is a set of source systems that are the core finance, risk and

treasury platforms to create authoritative transactional level and position

level data. The data structures, definitions and the update rates are often not

homogeneous in these systems because they are usually optimized to provide

operational processing, as opposed to regulatory reports. The architecture

views the linking of source systems as systems of record whereby original data

attributes are retained and required metadata necessary to support both

traceability and auditability of the downstream reporting lifecycle are

captured.

- Standardized ingestion layer: Standardized

ingestion layer is the layer that is in charge of sourcing out data in the

source systems and transforming it to a consistent and normalized format.

Initial validation checks, schema conformity, completeness and simple data

quality checks, are enforced in this layer, before the data is taken into the

regulatory pipeline. The architecture ensures the downstream is kept simple by

imposing common standards of ingestion and only allows data of the right format

to pass through the system in all ways such that its technology and governance

requirements have been defined in advance.

- Controlled reference data hub: The controlled

reference data hub is a central repository of important reference data that

contains legal entity hierarchy, product taxonomy, currency code, side of the

counterparty and so on. This layer gives uniformity of reference data within

all the processes of reporting and facilitates regulatory expectation of

similar interpretations of areas of significance. Reference data are placed

under strong governance, versioning and approval workflows to make changes

controlled and allow cumulative reproducibility of regulatory submissions.

- Transformation and aggregation layer: The transformation

and aggregation layer uses business rules, regulatory logic and calculation

methods in order to transform normalized source data into reportable metrics.

This layer facilitates intricate changes, such as currency converts,

risk-weighting, aggregations on legal entity levels and much more. Every logic

of transformation is recorded, parametrized and controlled to ensure

transparency and allow someone to trace the reported indices into their

underlying causes (regulators and internal stakeholders).

- Reconciliation and control

layer: The reconCIlation

and control layer is used to conduct organized verifications to confirm that

transformed data is valid. This involves balancing regulatory aggregates to

fund totals and ensuring consistency between such dimensions as legal entities

and products and unexplained variances. Hidden controls, tolerance limit and

exception management processes have been instituted to verify that

inconsistencies are investigated, registered and addressed before submission to

the regulatory authorities.

- Regulatory output layer: Regulatory output

layer will generate final submission ready reports and data files in a format

mandated by regulatory bodies. This layer can contain jurisdiction specified

templates, frequency of submission and validation regulations without detriment

of the underlying governed data set. Outputs are also completely audible,

reproducible and maintained with evidence of lineage and control, which allows

an institution to react properly to supervisory investigations and inspections.

3.2. Reference data controls

Reference

information, such as legal entity structures, product hierarchies and

counterparty classification, among other important dimensions13,14, contributes to the basic role of

regulatory reporting and resolution planning. The proposed architecture has the

reference data being consolidated through a controlled hub which acts as the

single source of authority to all the downstream regulatory processes. In

centralization, an imbalance manifested by duplicate or locally managed

reference datasets and disparity in the interpretation of key reporting

dimensions within the finance, risk and treasury boundaries is removed. As it

is a highly regulated data where the regulating body considers reference data

as defining the boundaries of aggregation and the factor to report on,

well-built governance and control systems are directly integrated in its

lifecycle management. All documentary data items will be tightly versioned and

effectively date to aid historical reproducibility of regulatory submissions. A

change is given the version identifier and time that it was made and the

business rationale that it was made and it is impossible to rearrange the data

that was actually used as references by any previous submission that was made

by the institution in history. This is essential to answer supervisor

questions, remediation work and lookback analysis, especially in resolution

planning, where the regulators can demand re-submission or recalculation of

past numbers in previous organizational set-ups. Reference data change

management is a formal work flow that involves two approvals, on both business

and data governance fronts. Changes are impacted to determine downstream

impacts on the logic of aggregation, its reconciliations and its regulatory

output before being further advanced to production. Segregation of duties takes

place through automated controls that cannot make alterations that are

unauthorized and also reduce operational risk. Besides, periodic attestations

and data quality checks are conducted to confirm completeness, accuracy and

consistency of reference data to outside sources and internal policies. The

architecture will facilitate the reproducibility of supervisory-perspective

regulation reports by integrating governance, auditability and reproducibility

into reference data management so that regulation reports are technically

correct and defensible on a supervisory basis. These controls, directly,

reinforce regulatory requirements of transparency, consistency and

explainability and they constitute an important enabler of dependable, scalable

and regulator-compliant reporting procedures.

3.3. Dual-control reconciliations

There are embedded

dual-control reconciliations in the regulatory reporting pipeline to verify the

integrity of the data it contains, its completeness and its defense to the

regulatory scrutiny15,16. Instead of

leading to a reconciliation as a single end-stage operation, the architecture

deploys checks at the transition points that are critical and independent

control perspectives are applied on the same stage. This method will allow

identifying the problems with data early enough, reduce the spread of mistakes

and leave documents by which they will be able to audit that they have checked

the reported numbers throughout the entire data lifecycle.

Figure 3: Dual-Control

Reconciliations.

- Source-to-ingestion reconciliation: The reconciliation

matches the data obtained by source, to ingestion ensures that all and all the

data extracted in the finance, risk and treasury source systems is completely

and purely mirrored in the standardized ingestion layer. Checks in this level

are based on the number of records, critical financial sums and such attributes

as legal entity, product and currency identifiers. The architecture will ensure

that no data is lost, copied or changed in the extraction and transfer process

since it reconciling the data ingested with source system control totals.

Errors are recorded and examined before reduced to downstream processing and a

firm basis on future transformations is established.

- Ingestion-to-transformation

reconciliation: Ingestion-to-transformation reconciliation is used to verify the

use of normalization rules and business logic when data is transferred to the

transformation and aggregation layer. The element of this stage here is to

determine the consistency of standardized data items following enrichment,

reference data merger and preliminary calculations. The controls involve check

of balance, dimensional completeness and verification of rules of

transformation against approved specifications. External validation of transformations

works well to ensure consistency in business and regulatory logic used in the

transformation processes and periodicity of business reports.

- Aggregation-to-output reconciliation: Aggregation-to-output

re-convergence is used to verify that the aggregated measures and regulatory

reports represent the underlying transformed data correctly. This involves

balancing regulatory totals to finance control figures, certifying

cross-dimensional consistency (legal entity/ product roll-ups) and certifying

consistency to regulatory templates. Tolerance levels and escalation protocols

are used to deal with acceptable tolerances and enquiry into abnormalities.

This last reconciliation levels offers a secure ensuring that the regulatory

submissions are indeed complete and are accurate with a definite audit trail

that links to the source and the output.

3.4. Deterministic aggregation logic

Deterministic

aggregation logic is an overarching design concept of the proposed regulatory

reporting architecture and acts as a guarantee that reported metrics are always

based on, can be fully explained and reproduced across reporting periods17,18. The aggregation policies are all

rule-based and parameterized and the business and regulatory logic is clearly

sped out and not hard-coded in an ad hoc script or custom tunings. Such a

strategy negates the use of discretionary overrides, which often introduce

operational risk and raise doubts among the supervisors and executes

standardized computations which are readily verifiable and effectively

reproducible. The aggregation rules are deterministic in nature i.e. to a given

set of rules; the same inputs should always have the same outputs. Other

important parameters like hierarchies in legal entities, conversion rate of

various currencies, reporting thresholds and regulatory classification mappings

are externalized off code and governed by controlled configuration tables. This

separation of parameters and logic increases transparency and gives the ability

to make changes controlled without necessarily having to redevelop, whilst

maintaining a clear audit trail of changes over time. All aggregation logic (rule

definitions, dependencies order of execution, etc.) is described and reconciled

with regulatory interpretations and governing internal policy. Aggregation

logic is formalized in version managed repositories having formal change

management and approval procedures that support auditability and supervisory

review. The versions of the logic are marked to which reporting periods are

applied, which makes it possible to recreate historical submissions accurately

and provide remediation or re-calculation requests to regulators. Robots’ tests

checks confirm the results of aggregation with specified situations and

balances without any risks of undesirable effects being applied in response to

changes. The architecture enhances the integrity of data and regulatory

defensibility by imposing deterministic and parameterized aggregation. It sees

to it that the results of aggregation are clear, repeatable and to the point of

business semantics and regulatory definitions. This ability is especially vital

in resolution planning and stress testing, where regulators are interested in

being assured that reported numbers can be brought into play on the necessary

scrutiny and within limited timeframes.

3.5. Testing and validation matrix

The testing and

validation system is designed in a multi-dimensional matrix, which is aimed at

providing holistic assurance of the regulatory reporting pipeline. Instead of

using one testing stage, the architecture uses a number of various types of

tests which are aligned to various areas of risk and give the architecture

correctness in both technical and regulatory sense. This stratified methodology

helps in the early identification of defects, manageable change process and

provide the traceable proof of rigor in testing so as to provide internal

control and audit.

Figure 4: Testing and

validation Matrix.

- Unit Testing: Unit

testing is a technique used to test single transformation rules and

calculations and data enrichment logic. All the rules undergo testing on

pre-defined scenarios of inputs and outputs to ensure to conform to the

documented business and regulatory needs. Unit tests test that transformation

logic is working as desired, responds to edge cases in a reasonable manner and

gives consistent results given work with known conditions. This test layer

enables defects to be curtailed at an early stage before they can trickle down

to lower aggregation and reporting operations.

- Integration Testing: The integration testing ensures that there are end-to-end data

flows between various systems and architecture layers, including ingestion of

data sources, transformation and reconciliation on the data to regulatory

output. The aim is to verify that data interfaces, dependencies and sequencing

are as expected when interaction between components occurs within a

production-like setup. Tests which verify schema compatibility, reference data

joins as well as cross-domain consistency, ensure that the pipeline is made to

work as a cohesive unity and not as a collection of independent modules.

- Regression Testing: To achieve stability and consistency in regulatory outputs despite

system enhancements, regulatory code change or infrastructure improvement,

regression testing is conducted. Regression testing detects the unintentional

impacts of changes by performing regression testing of previously tested cases

and situation comparisons. This is especially critical in a regulatory setting

where any slight deviation can attract questions of supervision or formal

clarification.

- Scenario Testing: Scenario testing is a method used to test behavior of the reporting

pipeline under pressure or hypothetical conditions used in the resolution

planning. Such tests measure how the aggregation logic and assumptions respond

to highly unlikely but possible situations, e.g. entity separability or

liquidity stress. Scenario testing aids in confirming the ability of the

architecture to uphold the regulatory prospects of stability and futuresight

test.

- Parallel Runs: Parallel runs Parallel runs are

operations that run the new reporting pipeline and compare the results to the

legacy processes in several reporting cycles. Analysis and the explanation of

differences and subsequent resolution are conducted to make integrity in the

new architecture. This method offers empirical demonstration of equivalence or

betterment, which contributes to controlled shift and control endorsement of

new reporting system.

3.6. Submission timeline and controls

A timeline that

comprises formal control gates that are meant to ensure there is accuracy,

accountability and regulatory compliance is controlling the regulatory

submission process19,20. Each of the

milestones of the timeline depicts an essential validation point at which the

data quality and the reconciliation state, as well as the governance approvals,

are confirmed before the next step is successful. this is a formalized method

of imposing a disciplined approach throughout the reporting chain and offers a

distinct indicative thread of control and decision making to internal audit and

oversight. When T-10 (Data Freeze) the source data is officially locked out to

the reporting period. Such freeze makes it consistent by avoiding the

introduction of changes which can compromise reproducibility and

reconciliation. All the data added on this level are versioned and tagged to

the reporting period to create a consistent baseline on the downstream

processing. Any exception or post freeze-adjustments may be stringently

escalated and approved and the nature of the reporting dataset is not

compromised. At T-7 (Reconciliation Signoff) all embedded reconcilments

throughout the pipeline, source-to-ingestion, ingestion-to-transformation and

aggregation-to-output must be engaged and officially examined. Exceptional

absences are enquired, clarified or clearly explained within justified

boundaries of tolerance. Independent functions of control offer checks on

whether figures which are reported have been reconciled to sources of authority

and adhered to standard practices of internal controls. At T-3 (Management

Certification) the senior management examines the final regulatory outputs,

supporting documentation and control evidence. Management certification will

ensure that submissions are complete, accurate and prepared as per what a

regulatory expects of submissions. The action strengthens accountability on the

right level of the organization and integrates the reporting outcomes provided

on the governance and risk supervision functions. At T (Regulatory Submission),

the final reports and data files are technically presented into the hands of

the regulator via established channels. Approvals, submission artifacts and

timestamps are stored to allow auditability and post-submission inquiries. All

these gated controls result in a clear, repeatable and regulator-ready

submission process which can stand up to supervisory review.

4. Results and Discussion

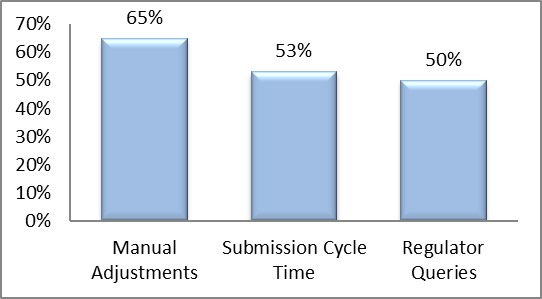

4.1. Data quality improvements

Table 1: Data Quality

Improvements.

|

Metric |

Improvement

(%) |

|

Manual Adjustments |

65% |

|

Submission Cycle Time |

53% |

|

Regulator Queries |

50% |

Figure 5: Graph

representing Data Quality Improvements.

- Manual adjustments (65% Improvement): The introduction of

the controlled, deterministic regulatory reporting architecture led to a huge number

of manual adjustments reduced. With the capability to build standardized

ingestion, controlled reference data, deterministic aggregation logic and

multi-layer reconciliations, a significant number of data anomalies that had to

be handled by people beforehand was removed on the fly. Robotic controls and

rule-based transformations minimized the use of spread sheets and hacks and

increased operational effectiveness and trust in the regulators. The fact that

the number of manual adjustments decreased 65 percent indicates a better degree

of data consistency, enhanced upstream data quality and greater execution of

control, on a reporting cycle.

- Submission cycle time (53% Improvement): By almost a half,

the time lag in submission cycles was selected to lessen, implying a decrease

in 15 days to 7 days per reporting interval. The reason behind this was the

fact that the data problems were earlier identified through embedded

reconciliations, the root-cause analysis was quicker due to end-to-end lineage

and less rework was required due to incorrectly fixed manually. The workflows

were streamlined, control gates were already preset and the financial, risk and

survived coordination across the finance, risk and treasury functions enhanced

the reporting speed. Reduced cycle times will increase the capability of the

institution to meet the shorter regulatory deadlines, especially stress or

resolution situations.

- Regulator queries (50% Improvement): Regulator questions

of data accuracy, consistency and explainability reduced by half post

implementation. Improved data lineage, version-controlled logic and extensive

documentation have allowed quicker and more accurate responses to supervisory

questions. Regulators could more easily use reported figures that have been

traced to authoritative sources and fewer follow-up clarification requests

would be necessary. Such a decrease suggests that transparency and

defensibility of submission regulatory reports are enhanced, which reinforces

supervisory trust and also reduces the currently experienced compliance levels

among reporting teams.

4.2. Audit and supervisory outcomes

Audited and

supervised reviews (after implementation) showed a significant level of

improvement in the transparency, reliability and defensibility of the

regulatory reporting process. Internal and external audit controls verified the

completeness of a full, end-to-end data lineage with the ability to report

figures that are traceable unambiguously back to source systems to ingestion

and transformation and aggregation through to ultimate regulatory reporting.

The metadata generated by the system, a version-controlled logic and a

timestamped control evidence helped to fill the void of the lineage

documentation and provided the ability to verify the correctness and integrity

of the reported information in a manner that is independent of manual

explanations or additional analyses. Better control efficacy was also observed

by the auditors in the purpose of the reporting lifecycle with references to

the areas of reconciliation, reference data governance and change management.

Buried reconciliations and explicit authorization processes minimized the

occurrence of undisclosed variance and the accurate recreation of submissions

in the past was achieved through good dating and versioning. Such possibilities

would help in mitigating the usual audit findings regarding data integrity,

inadequacy in documentation and inability to reproducely perform audits and

consequently reduce the amount of audit observations and re-mediation needs. As

a supervising aspect, regulators indicated an enhanced transparency and

effectiveness when it comes to examination and review. The standardization of

data definitions, deterministic aggregation logic and a rigorous lineage had

the important benefit of reducing the time needed to comprehend the reported

numbers and examine anomalies. Supervisory enquiries might be solved faster

because of the possibility to deliver uniform and well documented

clarifications with auditable support. This increased transparency boosted

confidence of regulators to the reporting system of the institution and ensured

that requests of data had to be repeated or follow-up reviews were lengthy. All

in all, the better audit and supervisory results indicate that the improved

efficiency of the operations is not accidental but, on the contrary, the

architecture contributes to the explainability, governance and control

regulatory expectations directly. This is especially essential in the context

of resolution planning, as regulators need to be extremely confident in the

capability of the institution to generate correct, prompt and justifiable data

when there is increased pressure and stricted deadlines.

4.3. Operational efficiency

The delivery of

automated reconciliation and deterministic aggregation logic has significantly

improved the productivity level of the operational aspects of the regulatory

reporting pipeline. The rule-based validations and systematic reconciliation

checks ensured on various levels, such as the source-to-ingestion,

ingestion-to-transformation and aggregation-to-output levels, helped to

decrease the number of steps that require manual work by subject-matter experts

to considerably. In the past, the complicated data problems and inconsistency

could easily involve intense scrutiny by finance, risk and treasury

professionals, leading to a point of congestion and resulting in an operational

risk associated with key-person dependency. The automatization and

standardization of processes are used to make sure that the tasks are performed

consistently, accurately and reproducibly and that fewer are utilized to these

processes, along with enhancing their overall resilience. Deterministic logic

also leads to efficiency in operative processes by eradicating discretionary

overrides and ad hoc calculations. All rules of transformation and aggregation

are parameterized, version-managed and well documented and the data may pass

through the pipeline without any manual reconfiguration. This does not only

increase the speed of the reporting cycle but also makes outputs predictable

and easy to audit. The architecture will eliminate the repetitive human effort

required and allow staff to work on activities associated with increased value,

including the analysis of exceptions, scenario planning and regulatory

engagement instead of daily data corrections or reconciliations. Combining

automated controls, embedded reconciliations and deterministic logic contribute

to lowering error propagation thus improving the reliability of upstream and

downstream processes. Reduced errors will lead to shortening of the cycle time,

average cut in regulatory inquiries and reworks, all of which can be tracked to

efficient gains. Also, the standardized processes enable scalability, so that

the institution can easily handle more and more volumes of data or more

regulation needs without corresponding staffing growth. All these operational

enhancements, in general, help the institution to make prompt, correct and

justifiable regulatory submissions and reduce the risks that come with

personnel dependency and manual processing. This leads to a more robust,

effective and sustainable reporting system that can respond to the changing

supervisory requirements and organizational expansion requirements.

5. Conclusion

The article posted

will describe a detailed, reconciled and traceable data pipeline system that

was dedicated to the FDIC resolution planning and high-frequency regulatory

reporting. The framework handles the key issues regarding contemporary

regulatory reporting, combining various levels of control, governance and

automation. Centralized reference data controls provide consistency, versioning

and an effective-dated reproducibility of important dimensions like the legal

entity, product hierarchy and counterparty classification. Multi-stage

dual-control reconciliations occurring between source-to-ingestion,

ingestion-to-transformation and aggregation-to-output confirm that the data

remains accurate and that anomalies are identified at an early age and supports

this information with auditing evidence to promote supervisor looking-glass

self-assurance. Deterministic aggregation logic is rule-based and

parameterized, version-controlled and documented and removes discretionary

overrides and produces reproducible results. In addition to these controls, a

formal testing and validating matrix, comprising of unit, integration,

regression, scenario and parallel testing is used, to ensure every part of the

pipeline is not only sound, but also reliable as well as in line with

regulatory expectations. Together, these contributions form a framework which

can produce audit ready, high quality regulatory information at scale and

shorten operational risk, cycle time and the use of subject-matter experts.

There is next

generation regulatory impact to the implementation of traceable and regularly

adjusted pipelines. With an ever-growing focus on transparency, reproducibility

and quick reaction to questioning on the part of supervisory authorities,

strong data pipelines are turning into a key part of the infrastructure, not a

superfluous improvement. The regulators are not only focusing on the accuracy

of the reported metrics but also on whether the institution can be able to show

full lineage including their ability to reconcile disparities and explain

variances as they arise in good time. Through adopting controlled,

deterministic and auditable reporting pipelines, institutions will be able to

address such increased expectations, increase the number of regulator queries

and enhance the trust in their reporting systems. Further, the architecture can

be used to ensure scalable compliance and to meet changing reporting

requirements, stress scenarios and resolution planning exercises without having

to make significant rework or draw on manual processes.

This framework can

be continued strategically in different ways in future research. The

incompatibility of reporting standards, legal entity structure and supervisory

expectations/ expectations across several regulatory regimes presents special

problems in cross-jurisdictional resolution planning and the framework would be

amenable to such complexities. Another frontier is real-time supervisory

reporting, potentially made possible by streams of data in high frequency and

automated controls that might permit near-instant reconciliation and submission

of regulations. Moreover, the adoption and adaptation with the new regulatory

technologies, including distributed ledgers, artificial intelligence-based

anomaly detectives and technological data provenance assistants, would

contribute to its transparency, predictive microeconomic efficiency and

capability. Considering these possibilities, the future of work might be

developed, basing on the basis of this paper, establishing regulation reporting

systems that are more robust, flexible and adapted to the changing environment

of the supervisory expectations.

6. References

- Supervision B. Basel committee on banking supervision.

Principles for Sound Liquidity Risk Management and Supervision, 2011.

- FSB. Key attributes of effective resolution regimes for

financial institutions, 2014.

- Bonollo M, Neri M. Data quality in banking: Regulatory

requirements and best practices. Journal of risk management in financial

institutions, 2012;5: 146-161.

- Khatri

V, Brown CV. Designing data governance. Communications of the ACM, 2010;53(1): 148-152.

- Otto B. Organizing data governance: Findings from the

telecommunications industry and consequences for large service providers.

Communications of the Association for Information Systems, 2011;29(1): 3.

- Buneman P, Khanna S, Wang-Chiew T. Why and where: A

characterization of data provenance. In International conference on database

theory, 2001: 316-330.

- Bovenzi JF. Inside the FDIC: Thirty years of bank failures,

bailouts and regulatory battles. John Wiley & Sons, 2015.

- Gordon M. Reconciliations: The forefront of regulatory

compliance procedures. Journal of Securities Operations & Custody, 2016;8: 356-363.

- Li J, Maiti A, Fei J. Features and scope of regulatory

technologies: challenges and opportunities with industrial internet of things.

Future Internet, 2023;15: 256.

- Bhatt T, Cusack C, Dent B, et al. Project to develop an

interoperable seafood traceability technology architecture: issues brief.

Comprehensive Reviews in Food Science and Food Safety, 2016;15: 392-429.

- Leuz C. Different approaches to corporate reporting

regulation: How jurisdictions differ and why. Accounting and business research,

2010;40: 229-256.

- Bowen F, Panagiotopoulos P. Regulatory roles and functions

in information-based regulation: A systematic review. International Review of

Administrative Sciences, 2020;86: 203-221.

- Marchini PL andrei P, Medioli A. Related party transactions

disclosure and procedures: a critical analysis in business groups. Corporate

Governance: The International Journal of Business in Society, 2019;19: 1253-1273.

- Kraakman RH, Armour J. The anatomy of corporate law: A

comparative and functional approach. Oxford university press, 2017.

- Bennett M. An industry ontology for risk data aggregation

reporting. Journal of Securities Operations & Custody, 2016;8: 132-145.

- Cai S, Gallina B, Nyström D, et al. Data aggregation

processes: a survey, a taxonomy and design guidelines. Computing, 2019;101: 1397-1429.

- Fang Z. System-of-systems architecture selection: A survey

of issues, methods and opportunities. IEEE Systems Journal, 2021;16: 4768-4779.

- Mahoney W, Gandhi RA. An

integrated framework for control system simulation and regulatory compliance

monitoring. International Journal of Critical Infrastructure Protection, 2011;4:

41-53.

- Bamberger KA. Technologies of compliance: Risk and regulation in a digital age. Tex L Rev, 2009;88: 669.

- Sparrow MK. The regulatory

craft: controlling risks, solving problems and managing compliance. Bloomsbury

Publishing USA, 2011.