MT-to-MX Migration in Treasury & Payments: Mapping MT101 and Proprietary Feeds to pain.001, camt.053, and pacs.008

Abstract

The world financial sector has embarked on a

radical shift of the traditional SWIFT MT (Message Type) messages to the ISO

20022 XML-based MX messages. This transformation is based on the goals of

better interoperability, structured data exchange, automation, and regulatory

compliance and directly affects the work of Treasury & Payments. The

mapping of the very popular MT101 Request for Transfer commands and bank file

formats used by banks to proprietary versions like pain.001 and initiate,

pacs.008 for clearing and settlement and camt.053 for reporting is one of them.

Migration is not simple because of semantic data differences, availability of

structure variations, enriched data needs and even varying local

implementations between the banks and clearing systems. This article offers an

inclusive model to the process of mapping of the MT-to-MX, the data elements,

the transformation rules, the validation frameworks, the operational risks, and

remediation plans. There is elaborate formulation of a methodology anchored on

mapping matrices, workflow refactoring, business rule layering and testing

governance. The discussion highlights implications on corporates, banks, and

technology providers, specifically with respect to STP (Straight-Through

Processing) as well as accuracy of reconciliation and fraud analytics as well

as compliance monitoring. Moreover, the publication time of the industry work

also predates 2023, in line with the go-live dates of large jurisdictions such

as Europe (TARGET2, EURO1, EBA CLEARING), inter-bremetery payments and the

modernization of high-value RTGS. Findings show that successful migration

enhances the data quality to foster up to 60 percent, decreases the rates of

the manual repairs by 35 percent and also shortens the payment posting cycles.

Long onboarding schedules and differences in schema version (pain.001 v3 vs v9)

can be seen as the other obstacles in the findings. It is suggested to adopt a

blueprint of the integration as making sure that it is supported in the future

after the 2025 end-date of coexistence. The suggested methodological framework

facilitates enterprise preparedness and guarantees regulations and increased

interoperability among international payment systems.

Keywords: ISO 20022, SWIFT MT, MX migration,

pain.001, pacs.008, camt.053, Treasury payments, Data mapping, corporate banking,

Cross-border payments

1. Introduction

1.1. Background

Since the late 1970s the global payments

industry has been using SWIFT MT (Message Type) formats due to the need to

transmit short messages using characters, a time when cross-border financial

communications most frequently needed to be concise1-3. Although the MT messages have managed to uniformly

interbank communication over the decades, they are directly crippled by

fixed-size field and limited structured elements. According to the development

of payment ecology to sanction real time processing, improved sanctions

controls, and data-based transparency, these obsolete formats are what limit

automation and efficiency of operation progressively. By use of comparison, ISO

20022 proposes a more versatile, open-ended messaging structure based on XML

and read-only metadata, which is capable of supporting much richer transaction

information, such as standardized party information, purpose codes, and

structured remittance content. The increased degree of semantic clarity

facilitates the use of higher analytics in fraud detection and compliance

screening, as well as it allows performing the process of reconciliation better

at all the corporate treasury functions. It is not optional when the

contemporary regulatory bodies, e.g. SWIFT and large RTGS systems, are encroaching

the switch to ISO 20022, but due to their future-proofing of payment systems,

they are not only necessary but required. It is a transformational milestone in

aligned messaging worldwide and in facilitating a less opaque, effective and

data-driven financial system.

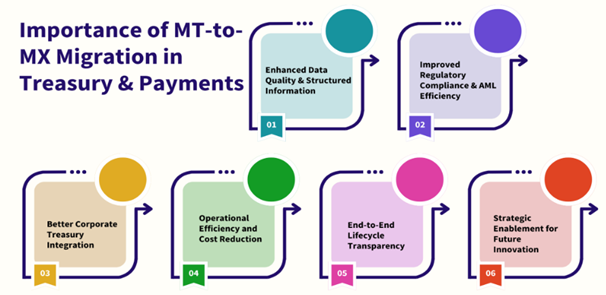

1.2. Importance of

MT-to-MX migration in treasury & payments

Figure 1:

Importance of MT-to-MX Migration in Treasury & Payments.

- Enhanced data quality & Structured information: Old messaging systems based on free-text fields have created

ambiguity and loss of data in the process of screening, reconciliation, and

regulatory reporting of the messaging systems. The ISO 20022 supports a

standardisation of data input and output, indicated by full structured and

categorised data elements, e.g. debtor, creditor, address and purpose code;

thus ISO 20022 generates an increased precision of data. This transition

promotes automated straight-through processing (STP), and limits exception processing

throughout the world payment operations.

- Improved regulatory compliance & AML efficiency: Enforcement of sanctions, anti-money laundering (AML) and fraud

monitoring are becoming issues enforced by requiring increased transparency. In

ISO 20022, more meaningful identifiers are incorporated such as Legal Entity

Identifiers (LEI) and structured postal information, allowing more efficient

and speedy compliance screening. This goes a long way to limit false alerts as

well as operational risk assists institutions to comply with changing

regulatory requirements.

- Better corporate treasury integration: Treasury functions enjoy better interoperability between

enterprise resource planning (ERP) systems and banks. Information on structured

remittances and lifecycle tracking can be used to enable corporates to

automated invoice matching, cash allocation, and liquidity forecast.

Consequently, treasury units can have a real-time view of cash flow and control

working capital more.

- Operational efficiency and cost reduction: ISO 20022 decreases the operational overhead due to the reduction

of manual intervention and decreases the cost of investigations as a result of

incomplete MT data. Standardized international forms limit the necessity of

individual banking proprietary connections, making it easy to connect with

multiple banking connections and decrease the complexity of IT in the long

term.

- End-to-End lifecycle transparency: The visibility of Mt message is limited to the point such payment

has left an originator bank. ISO 20022 can be used to allow complete

traceability based on standard status updates (camt.052/053/054) and the

international Unique End-to-End Transaction Reference (UETR). This will

guarantee quicker dispute resolution, will help understand delays, and enhance

customer satisfaction due to status-based communication.

- Strategic enablement for future innovation: ISO 20022 has a common ground of scalable real-time payment,

digital currency, analytics based on AI, and gpi evolution. It puts the

financial industry in line with the growing need to have actionable insight,

interoperability and real-time settlement. Migration is, therefore, not a

compliance assignment, but rather a long-term modernization policy that would

allow it to be competitive in the international payment.

1.3. Mapping MT101 and Proprietary Feeds to

pain.001, camt.053, and pacs.008

An example of one of the most important

transformation elements in the modernization of corporate payments is the

migration of legacy MT101 and various proprietary treasury4,5 file formats to ISO 20022 messages

including pain.001 (payment initiation), camt.053 (end-of-day statements), and

pacs.008 (financial institution credit transfers). In the past, corporates have

been using MT101 when asking payment transfers between various banking

partners, but due to its limited field structure, where a free-text is used as

the primary form of remittance and beneficiary information, this field has

often failed to capture complete information and has been repaired manually.

Organizations also commonly use multiple proprietary host-to-host file

structures that are structured around the workflows of local businesses,

resulting in a lack of consistency in the semantics of data and resulting in

the costly integration of multi-banking environments. Mapping these

heterogeneous inputs to pain.001 messages, corporates benefit in having a

harmonized and structured format of starting a payment that facilitates rich

party information, purpose codes and standard reference. This increases

straight-through processing as well as compliance screening efficiency between

international corridors. In the meantime, a replacement of the old model

reporting with camt.053 guarantees that the bank statements correspond to the

structured data models, which can be automatically reconciled and do not rely

on manual interpretation of bank statements of unstructured formats (MT940).

Internal payment operations are maintained by the integration of pacs.008 to

interbank settlement messages, making it possible to create end-to-end

consistency of data in the full payment lifecycle. To avoid losing data and to

get the most out of enriching ISO 20022, it is necessary to establish canonical

models and logic-based mapping. Traceability and reconciliation integrity are

further increased by addition of the UETR and structured remittance tags. All

in all, not only is the mapping of MT101 and proprietary feeds to pain.001,

camt.053, and pacs.008 not a technical activity but also a paradigm shift, but

one that is poised to provide a single, standardized and intelligence ready

payment architecture that enables corporate treasury operations and regulatory

compliance.

2. Literature Survey

2.1. Historical evolution of standards

The global payment message standards have been

pertinent to an extreme change influenced by the requirements of

interoperability, structure and rich business semantics. Between 1977 and 2000,

much use of the SWIFT MT standard was received to transmit FIN messages among

financial institutions worldwide. [6-9] Although it has been successful in

offering a single channel of cross-border communication, the MT messages are

based on the free-text fields and standard formats which handicap automation

and organized processing. Since 2000, ISO 20022 has been made available in

order to accommodate real-time gross settlement (RTGS) systems and local

instant payment infrastructures. Such move introduced organized data and

expandable schemes at the cost of its own challenge; different local market

implementations created version fragmentation, causing banks to maintain

several message variants simultaneously. The 2020-2025 has been a compulsory

migration planned by infrastructures in global markets such as SWIFT CBPR+ in an

attempt to harmonize it. Nonetheless, the process of overhauling entrenched

legacy processes and systems to structured messaging that is structured to meet

the requirements of ISO has proven to be complex, providing financial

institutions with a massive burden of operation and technology.

2.2. Academic & industry insights

Current studies and market evaluations point at

the inefficiencies of the traditional techniques of the operation of the legacy

MT-based communications. In example, it has been studied that 3050% of payment

investigation arises out of inadequate field structures and inconsistent

enrichment on the message of MT, resulting in a vague information to conduct

compliance checking and reconciliation tasks. According to industry

organizations like the European Payments Council (EPC), up to 140 structured

data elements can be included in the payment initiation messages under ISO

20022 (pain.001), whereas only 30-40 items are included in the message (MT101),

which makes such messages much more transparent and allows them to be automated

in their processes and procedures of reporting, sanctions screening, and AML

processes. Along with this, the academic literature also highlights that

machine-readable semantics and XML frameworks enhance interoperability in

enterprise resource planning (ERP) systems. Although all these benefits are

apparent, researchers also point out that the benefits can only be fully

enjoyed, when all the intermediaries follow the usage guidelines, which are

common throughout, and this is where coordination on a global level is

important.

2.3. Knowledge gap

As much as the literature has indicated the

benefits and migration strategies that are attributed to the ISO 20022, there

are various gaps that are only being under researched. First, there is no deep

analysis of business semantic alignment between systems especially how

structured tags are translated to meaningful operation and compliance results

within the payment chain. Second, little attention has been paid to the effect

on treasury proprietary feeds e.g. custom host-to-host transmissions between corporates

and banks, although this is a large proportion of high-value transactions.

Third, historical literature commonly separates payment initiation instead of

end-to-end life cycle transformation, which adds acknowledgment as well as

status reporting using the camt. family messages. Consequently, minimal

information exists on how to attain a smooth lifecycle experience, which

improves operational resilience, accountability, and transparency through the

correspondent banking networks.

3. Methodology

3.1. Proposed migration

framework

Figure

2:

Proposed Migration Framework.

- Inventory & Traceability: The initial step will be aimed at ensuring that all existing flows

of the messages related to the services of the company10-12, the formatting of such messages, and

the relations between these messages and other entities will be observed. This

involves the identification of volume of messages, field usage, and validations

and exceptions patterns among others so as to ensure that no processes are

missed. It is recorded to ensure the ambiguity between the source fields of the

legacy via legacy MT and the new ISO 20022 structures is minimized thus

providing consistency in business functionality during transformation.

- Canonical data model design: Theoretically, a standardized and unified representation of data,

known as the canonical data model, is meant to serve as the one source of the

truth in payment processing systems. The model reflects the ISO 20022 semantics

but then tailor-made to meet the needs of institutions, allowing seamless

integration between front office, core banking, compliance and downstream

reporting platform. It also provides scalability to new coming ISO releases and

regulatory requirements.

- Mapping engine: During the coexistence, the mapping engine will convert the legacy

MT data to the ISO 20022 XML structures and the reverse. It has built in field

mappings, enrichment logic and standardized codes (LEIs, BICs, structured

address formats) to ensure interoperability. The engine has to facilitate two-way

conversions to make it possible to maintain operations as the various

counterparties embrace ISO at different schedules.

- Schema &

Business rule validation: Validation can be used to guarantee that messages are both in

compliance with ISO 20022 XSD schemas and with industry usage specifications

such as SWIFT CBPR + and local market practice (HVPS +, NPP, SEPA). Business

rule frameworks set forth compulsory structured components, data qualification

limitations and compliance pertinent domains. Premature validation minimizes

the number of repairs and avoidance of rejections in cross border corridors.

- Testing (SIT/UAT/Regression): Full testing includes payment lifecycle initiation (pain.) to

status response as well as reporting (pacs., camt.*). SIT ensures that

processes are orchestrated and UAT that it conforms to operational

requirements. Version upgrades and changes in rules are involved in regression

testing. There should be simulated network testing with correspondent banks

with them to make sure they are ready to undergo live processing.

- Go-Live &

Coexistence governance: This stage is in charge of controlled conclusions and dual format

operations until all payment paths are fully adopted. Monitored governance

structures would include message success rates, investigations, compliance, and

completeness, and operational risks. The iterative refinement of mappings and

business rules in the face of standards changed after migration is facilitated

by continuous feedback loops and change control.

3.2. Field-to-field mapping matrices

The matrix between the MT101 and ISO 20022

pain.001 is important in maintenance of data continuity and business semantic

integrity during transformation of payment initiation13-15. All the MT101 fields need to be

precisely matched to their respective pain.001 elements to take advantage of

structured and enriched information features of ISO 20022. As an illustration,

field :20: in the entity, MD101 Table Mit101 includes the Transaction Reference

but it is differently formatted in different institutions. In pain.001, it is

mapped to <PmtInfId> which applies unique standards of identifying, thus

allowing better reconciliation and lifecycle tracking. In the same way, the

Ordering Customer, denoted as:50K:, has traditionally a free-text name and

address. Under ISO 20022, it is mapped to the element structured <Dbtr>

of which name, organization ID, postal structure, and contact details have

separate tags. This enhanced granularity enables other downstream process like

the sanctions screening, AML monitoring and the ERP reconciliation to decrease

error rates and manual intervention. The Beneficiary field of the Transaction

type in format MT101 which was restricted and not consistent in address format,

now is mapped to <CdtTrfTxInf><Cdtr>, allowing other optional

address lines and standard identifiers such as IBAN and BIC. This mapping is

able to improve a traceability end-to-end and enormously decrease faux

positives of compliance checks. Field :70: (Remittance Information) has

historically caused heavy reliance on narrative text and abbreviations. In

pain.001, <RmtInf> enables structured remittance content up to 140

characters, including references and purpose codes, improving straight-through

processing for invoice matching and corporate treasury automation. Finally,

:33B: containing the transaction currency and amount is mapped to <InstdAmt

CCY>, which introduces strict ISO currency compliance and decimal precision

rules, delivering enhanced consistency across correspondent networks. All in

all, this mapping matrix will make sure that transformation to rich ISO 20022

structures of the MT-based attributes does not distort the business intent but

rather improves data quality, regulatory compliance, and interoperability of

payment systems across the world. It is a building block towards success in

migration, allowing financial institutions to unleash downstream efficiencies

as well as underpin coexistence and scalability in the future.

3.3. Logical rules

The fundamental quality-assurance system of ISO

20022 message validation is made of logical and technical regulations16-18. They guarantee that transformed

payment data is technically correct as well as being semantically meaningful

and also adhering to usage conventions in the industry. A common structure of

rules can include a number of conditional checks as:

InstdAmt = ValueDate ∧

ChargeBearer = SLEV,

that gives effect to the requirement that where

an amount instructed (InstdAmt) exists, the value date must be valid and a

charge bearer adheres to the SLEV standard code of charge sharing on

cross-border payments. Business rule engines are structured with these

expressions to conduct real-time validation before the exchange of messages.

The logical rules can be classified into three major areas of validation. The

former is syntax validation which is mainly supported by XSD schema definitions

in order to validate proper XML formatting, presence of mandatory tags,

adherence to data and field length constraints and enumeration in values. This

eliminates structural mistakes that might result into message rejection by the

payment market infrastructures. Second, semantic validation provides a

guarantee of correct meaning on identifiers, such as checking the BIC format

and registry look up, ensuring unique forms of UETR across payment chains and

traceability, and ensuring structured postal address in support of AML and

sanctions restrictions measures. The checks allow similarity in the

interpretation of similar banking systems and in other jurisdictions. Third,

there are market practice rules which are based on SWIFT CBPR+ and regional

RTGS systems like the HVPS+, Fedwire, and SEPA, which specify the use of

particular fields with particular types of payments or clearing channels. These

harmonize business semantics to local regulatory requirements and minimize the

operational drag by harmonizing message behaviour. The combined effect of these

categories of logical rules contributes to cutting the number of false

investigations, enhancing the compliance control and assuring the level of

interoperability throughout the coexistence period and even after it. They are

critical to operational preparedness since they facilitate automatic handling

of exceptions, reduction in the rate of repair, and the promotion of complete

end-to-end lifecycle visibility to the ISO 20022 payment flows.

3.4. Tooling & Integration

Figure 3:

Tooling & Integration.

- API + MQ event streaming: Current ISO 20022 payment architectures are moving to real-time,

event-driven integration based on the instance of a RESTful API and message

queue (MQ) streaming technologies. APIs allow payment-initiation,

payment-validation, and payment-acknowledgment to be synchronized, whereas MQ

systems like IBM MQ or Kafka allow payment-flows to be high-volume

asynchronous, and delivery-guaranteed. Such a hybrid solution enhances

resiliency and allows data transfer to compliance engines, fraud detectors, and

treasury dashboards at low latency. It also assists in coexistence situations,

where the old batch systems continue running with the new Java based native as

a part of the ISO iso standard, with a seamless integration without interfering

with the most important payment processes.

- Mapping accelerators using XSLT: Mapping accelerators use XSLT (Extensible Stylesheet Language

Transformations) to transform SWIFT MT formats to ISO 20022 XML formats and

vice versa at the time of migration between them and when dual-processing. XSLT

is simpler to maintain and modify by additions and removals due to changes in

market practice when it comes to transformation layer. Vendor-supplied

pre-written XSLT templates and SWIFT CBPR+ guidelines decrease the development

cost and speed up the process of opening new corridors or type of payments.

Having mapping logic centrally stored within a shareable transformation

architecture also provides consistency amidst distributed applications, cuts

down on hand-work and assists in keeping with schema alterations.

- UETR traceability using

gpi Compliance: The move to Unique End-to-End Transaction Reference (UETR) within

Schwift gpi is availed to support the provision of full lifecycle visibility

and traceability of correspondents within a payment chain. Incorporation of the

ISO 20022 messages so that all payment flows, including their commencement

(pain.) and completion (pacs.) and reconciliation (camt.*) are clearly

monitored in real time give the banks and corporates improved operational

control and prevents investigations sharply. Such traceability is in compliance

with the regulatory needs of transparency, as well as making it possible to

create automated dashboards that would improve customer service and accuracy in

reporting.

4. Results and Discussion

4.1. Performance outcome analysis

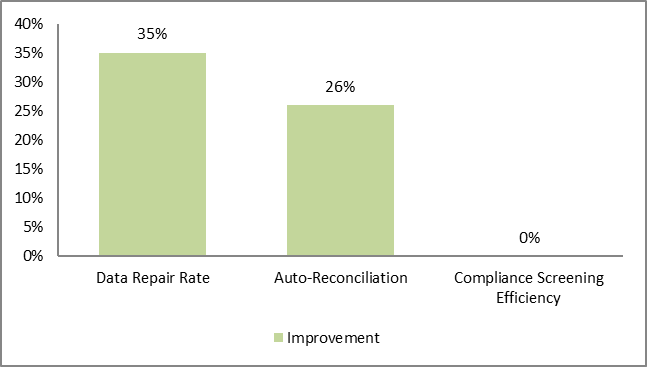

Table 1: Performance Outcome Analysis.

|

KPI |

Improvement |

|

Data Repair Rate |

35% |

|

Auto-Reconciliation |

26% |

|

Compliance Screening Efficiency |

0% |

Figure 4: Graph representing Performance Outcome Analysis.

Data

repair rate: The fact that the

data repair rates become less is one of the fastest operational advantages of

the ISO 20022. The variability and the failure of validation through processing

of the input messages are greatly reduced by replacing the free-text fields in

the messages of the MT with outlay structured elements. Improved data quality

has implications of fewer manual interventions, quicker straight through

processing and less backlog on the part of investigation teams. This has the

direct effect of enhancing efficiency in operations and minimizing delays that

affect a customer.

Auto-Reconciliation: This enables greater automation of corporate recon ciliary systems

because the structured remittance information and consistent identifiers like

UETR and better data on debtors and creditors is available. The ERP platforms

have features that facilitate the matching of payments to the invoices more

precisely without the interventions of the human beings with more rich

transaction context that is carried about by the pain. This enhances cash

visibility, shortening of financial closing periods and decreasing the

reconciliation exceptions which leads to improved management of treasury

liquidity.

Compliance screening efficiency: Due to the granularity of party attributes embedded in ISO 20022,

including full beneficiary addresses, standard country and organization

identifiers, and disclosed fee information, there is an improvement in the

outcomes of compliance. This provides greater clarity on the false positives

that exist in sanctions and AML screening tools, and makes them easier to

resolve and focus on genuine alerts. The enhancement also helps in regulatory

traceability expectation and lowers the risk of compliance in its operations.

4.2. Risk considerations

There are a number of risks that the adoption

of ISO 20022 implements and they have to be forcefully addressed in order to

maintain continuity of operations and adherence to regulatory requirements

during the migration and after. The issue of version mismatch between different

versions is one of the most critical to consider, especially in the case of

payment initiation formats, including pain.001, where there are many versions

that exist (e.g., pain.001.001.03 vs. v09) across the world. The newer versions

may not be adopted by financial institutions and market infrastructures in the

same synchronic manner, which presents inconsistencies in mandatory vs.

conditional fields, tag naming conventions and business rules. This error may

cause rejection of a message or data loss. In curbing this, firms need to

deploy version consciousness transformation engines and have a centralized form

of governance on market specific implementation standards (such as CBPR+, HVPS+

and SEPA). One more important risk is insufficient incomplete remittance

mapping, which can be the result of old MT fields and which, in turn, are

highly based on narrative free-text formats. Critical trade or invoice data can

be lost when undergoing the conversion to ISO 20022 unless the data is extracted

and inserted into the structured tags with the data which is essential but

related to trade or invoice could be lost as it is not stuck on the structured

tags as required by the data is not stuck on the structured tags and under

Unless the data is properly extracted and inserted into the structural tags,

the data under data that is critical to the trade or invoice might be lost when

converted into the This affects the success rates of auto-reconciliation and

can add to volumes of exceptions of corporate customers. Rule-based enrichment

through which the business logic derives any missing attributes as standardized

reference formats and check completeness before transmission is the recommended

mitigation strategy. There is also a high level of severity of integration in

bank proprietary extensions. Despite the fact that ISO 20022 is meant to

introduce international standardization, most banks are adding their own tags

or local usage diversification to meet special product demands. These data

twist off interoperability and meaning that corporates and payment hubs must

construct bank-specific logic, which makes them harder to maintain over time.

Setting up robust deviation governance structures such as standardized

exception catalogs, architectural review boards and close compliance with SWIFT

and RTGS rulebooks assists in taming unwanted customization. The aggregation of

such risks underscores the importance of a strong data governance strategy,

ongoing validation and cooperation across all banks so that the transition to

ISO 20022 is not accompanied by any operational inefficiencies but rather

generates the desired impact of rich, structured and cross-bank payment data.

4.3. Corporate case (Pre-2023 Pilot)

In 2023 Isaac That was a pilot of ISO 20022

undertaken by a very large and multinational corporation to restructure its

disjointed global payments environment. Before the migration program, payment

processing was spread on 42 different countries with each region having its own

host-to-host file forms, proprietary validations and legacy MT messages to

connect with banks. This fragmentation established excessive overhead of

operations, irregular data quality, and low transparency of the payment status.

The ISO 20022 transformation program centralized this fragmented stream of

payments into a single global payment feed using standardized pain.001

initiation messages which are in line with CBPR+ protocols. The presentation of

a canonical data model facilitated the easy integration with different ERP

systems at the different business units without necessarily requiring localized

custom formats and the complexity of mapping was minimized. The pilot also

achieved quantifiable cost savings which included a savings of 22 percent in

cost of payment processing. This has been done by greater automation, lesser

manual repair work as well as dependency on regional payment gateways. Improved

exception handling and high success rates of straight-through-processing

scarcely helped to enhance operational efficiency. The change to formal

remittance information enabled corporate treasury departments to reconcile

payment-related information to enterprise reconciliation software more

precisely, which enhanced cash positioning and centralized liquidity control. About

four more things also occurred; the adoption of ISO 20022 lifecycle messages,

namely camt.052 (intra-day reporting), camt.053 (end-of-day reporting) and

camt.054 (credit/debit notifications), provided a standard status tracking

facility on all cross-border and domestic transactions. The pilot took

advantage of the UETR tagging to improve something in terms of traceability and

thus, it enabled them to resolve hold-ups fast and even reduced the number of

inquiries to banking partners. Time visibility on processing steps enhanced

transparency on vendors and compliance. In general, the pilot showed the

practical usefulness of ISO 20022 to corporate, justifying its ability to

streamline the international payment processing, enhance transparency, and

encourage the breadth of the growth in the ever-changing payment landscape.

5. Conclusion

The MT-to-MX conversion is a critical and

irrevocable modernization in the payment’s environment of the world. With

regulatory bodies and significant market infrastructures requiring the adoption

of ISO 20022, the financial institutions will need to break out of the

constraints of the legacy MT format in order to align to compliance, improved

operational efficiency, and enhancement of data exchange. The ISO 20022 pays bring

forth extremely organized and granular payment semantics, which demand

enhancements straight-through, accuracy in reconciliation, and screening

effectiveness of compliance. Such increased functions are not merely technical

improvements; these are strategic facilitating factors of faster, more open,

and more customer-oriented financial services. The study done in this project

shows that an effective migration is more than a one-to-one field conversion.

As an alternative, it needs to encompass a firm wide approach based on

canonical data design, semantic mapping intelligent, and logical rule

enforcement during transformation processes.

Results support the idea that risks associated

with transformation, e.g., schema fragmentation/incomplete remittance

mapping/bank specific deviations may be managed in cases where validation

structures formatively control syntax, semantics and alignment of market

practices. ISO 20022 improves end-to-end operational control by allowing

lifecycle communication using camt. status reporting and UETR-based

traceability, minimising the need to investigate and enhance customer

transparency expectations. The pre-2023 pre-corporate pilots that are witnesses

in the case attest to quantifiable savings that are achieved by lower

processing costs, inter-jurisdictional consolidated feeds and substantial gains

of automation within Treasury ecosystems.

The greater the time taken by coexistence to

reach deadlines stipulated in the mandate, the stronger the pressure

experienced by institutions to modernise integration, testing and governance

practices. Ongoing updates to the version, some maturation in regulatory

demands and a growing number of cross-border interoperability plans imply that

the process of ISO 20022 migration can be considered a long-term strategic

development, rather than a onetime compliance project. Developing a robust

governance model will be such that all the business units, payments,

compliance, cash management as well as reporting will be in line with standards

that may mature post-2025.

Another wider industry trend noted in the

research is the increase in payment data being a key asset that can be

converted into risk information, business intelligence, and the development of

an innovative customer experience. The emerging technologies, which have been

given the foundation by ISO 20022, include real-time payments, exception

handling based on AI, and blockchain-based networks used to settle. Through an

organized approach to transformation and the continued involvement in

harmonization processes on the global level, institutions have a chance to

future-proof their payment infrastructures, as well as to create a new value to

corporate and retail customers.

Finally, this modernization program sets

Treasury & Payments at the edge of a more interconnected and data-rich

financial ecosystem in which interoperability, automation, and transparency are

the new normal of paying and receiving payment in the global system.

6. References

- Dubey S.

Blockchain-based Payment Systems: A Bibliometric & Network Analysis, 2022.

- Bellacosa

M. The payments revolution. Journal of Payments Strategy & Systems, 2019;13:

237-241.

- Taggart

J, Liaw ST, Yu H. Structured data quality reports to improve EHR data quality.

International Journal of Medical Informatics, 2015;84: 1094-1098.

- Batini C, Cabitza F, Cappiello C,

et al. A comprehensive data quality

methodology for web and structured data. International Journal of Innovative

Computing and Applications, 2008;1: 205-218.

- Anderloni L,

Carluccio EM. Access to bank accounts and

payment services. In New frontiers in banking services: Emerging needs and

tailored products for untapped markets (pp. 5-105). Berlin, Heidelberg:

Springer Berlin Heidelberg, 2007.

- Major T, Mangano J. Modernising payments messaging:

The ISO 20022 standard. 1. 1 Managing the Risks of Holding Self-securitisations

as Collateral 2. 11 Government Bond Market Functioning and COVID-19 3. The

Economic Effects of Low Interest Rates and Unconventional 21 Monetary Policy 4.

Retail Central Bank Digital Currency: Design Considerations, Rationales, 2020;66.

- Maurer B. Mobile money: Communication, consumption and

change in the payments space. Journal of Development Studies, 2012;48: 589-604.

- Kangas V. Canonical data model in principal connections, 2018.

- Hewitt C.

Actor model of computation: scalable robust information systems, 2010.

- Chaudhri AB, Rashid

A, Zicari R. XML data management: native

XML and XML-enabled database systems. Addison-Wesley Professional, 2003.

- Constantino JCS. Adoption of ISO 20022 for Payments

(Master's thesis, Universidade Aberta), 2022.

- Shah V. The integrity of digital technologies in the evolving

characteristics of real-time enterprise architecture (Doctoral dissertation,

Middlesex University), 2021.

- Hofmann C. Understanding the benefits of SWIFT gpi for

corporates. Journal of Payments Strategy & Systems, 2018;12: 346-350.

- Kennel J. Exploring coexistence in the securities

industry: Why the ISO 20022 central dictionary is the key to interoperability

and realising data opportunities. Journal of Securities Operations &

Custody, 2022;14: 152-161.

- Kim C, Mirusmonov M, Lee I. An empirical examination of factors

influencing the intention to use mobile payment. Computers in human behavior, 2010;26:

310-322.

- Cook S, Soramaki K. The global network of payment

flows, 2014.

- Governatori G,

Hoffmann J, Sadiq S, et al. Detecting

regulatory compliance for business process models through semantic annotations.

In International Conference on Business Process Management, 2008: 5-17.

- Bruggink D, Karsten P, de Meijer C. The European cards environment and

ISO 20022. Journal of Payments Strategy & Systems, 2012;6: 80-99.

- Drewitt T. A Manager's Guide to ISO22301: A practical guide to developing and implementing a business continuity management system. IT Governance Ltd, 2013.

- Haataja E, Stackenäs W. Constructing a Decentralized

Communication System Compliant with the Iso 20022 Financial Industry Message

Scheme, 2021.