The Future of Finance: AI-Driven Innovations in CRM, Cybersecurity, and Banking Ecosystems

Abstract

Artificial

Intelligence (AI) is currently on the path of transforming the financial sector

with AI-based Customer Relationship Management (CRM), cybersecurity and

financial banking ecosystem. Predictive analytics, personalized

recommendations, and automated support from AI-powered CRM systems give

customers faster and better customer engagement, which enhances customer

retention and makes operations more efficient. Machine learning and real-time

anomaly detection are changing threat detection, fraud prevention, and risk

assessment to use in cybersecurity, as well as using AI to mitigate cyber

threats with unheard-of accuracy. At the same time, AI is disrupting the way

banking ecosystems are being redefined to offer hyper-personalization of

financial services, optimization of credit risk models, and even more efficient

regulatory compliance. In this paper, we first examine how AI impacts these

critical areas and how financial institutions employ AI to innovate, protect

security, and improve the customer experience.

Furthermore,

it also speaks about the problems of AI adoption, such as ethical concerns and

data privacy problems, among others. With the ongoing development of AI,

financial institutions pay attention to the admission of the process between

innovation and compliance and disclose loyalty and trust. The integration of AI

will be key to the strategic future of finance and a more secure,

customer-centric, and resilient financial landscape.

Keywords: AI in

finance, Customer Relationship Management (CRM), Financial cybersecurity,

Banking ecosystems, Machine learning, Fraud detection, Predictive analytics,

Risk assessment, Regulatory compliance, Digital transformation

1.Introduction

Digital

transformation in the financial sector focuses on Artificial Intelligence (AI)

to transform conventional operations. From Customer Relationship Management

(CRM) to areas like the banking ecosystem, cybersecurity, and so on, AI-driven

innovations are redefining what it means to engage with customers, secure

transactions, and optimize financial services by financial institutions1-4. With the

approach of AI adoption by financial institutions, they need to address the

issues of data privacy, compliance, and ethical adoption of AI.

1.1.

AI in Financial Services: A Paradigm Shift

Artificial

Intelligence (AI) is revolutionizing the traditional financial sector, and

digital transformation is at the forefront. AI transforms banking ecosystems by

transforming how financial institutions interact with customers, securing

transactions and providing financial services. Faced with financial

institutions embracing AI, one must also grapple with data privacy, regulatory

compliance, and ethical AI adoption.

1.2.

Enhancing Cybersecurity with AI

With

financial transactions transacted more digitally, stupidity on attacks has

evolved to be more complex. The AI-enabled cybersecurity solutions leverage

advanced analytics, real-time monitoring, and predictive modeling to identify

and stop fraud, data breaches, or cyberattacks. Financial institutions can use

AI-enabled security frameworks to analyze large datasets and anomalies and

combat these risks before they cause damage. Trust and trusted sensitive

financial information are maintained by the application of AI in cybersecurity.

1.3.

AI’s Role in Modern Banking Ecosystems

AI-driven

financial innovation is shaping the future of banking ecosystems, such as

AI-powered hyper-personalized financial services, automated credit risk

assessments and real-time fraud detection. However, customer experience

continues to be revolutionized by AI-powered chatbots, robo advisers and

predictive analytics, as it maximizes operational efficiency. Furthermore, AI

is automating regulatory compliance to uphold financial regulations and reduce

the cost of complying with them.

2. AI in

Financial Customer Relationship Management (CRM)

Artificial

Intelligence (AI) is making its way into the financial sector to change

customer relationship management (CRM) and make institutions provide seamless,

personalized, and informative services. AI in CRM systems uses advanced data

analytics, machine learning, and automation to enhance customer interactions,

optimize engagement strategies, and improve overall customer satisfaction5-8. The innovations resulting from these

financial services not only streamline the process but also allow financial

institutions to create stronger relationships with their customers,

consequently supporting a higher level of customer loyalty and overall

financial growth.

2.1.

Role of AI in Enhancing Customer Experience

2.1.1.

AI-Powered Chatbots and Virtual Assistants

AI-powered

chatbots and virtual assistants are becoming basic in financial CRM. These AI

systems interact with customers in a human-like manner by using NLP machine

learning algorithms. 24/7 on hand, they answer queries, process transactions,

and advise customers through account management tasks. With this availability,

the customers’ experience is greatly improved since there is an immediate

response outside regular business hours.

AI-driven

virtual assistants allow financial institutions to become more independent of

human agent services so that they can devote their time and effort to more

complicated questions. Chatbots answer routine questions but continue to learn

from customer interactions using machine learning to improve responses. It

saves time and leads towards reduced operational costs over time. This means

faster, more accurate customer service, and they will be satisfied.

2.1.2.

Personalized Financial Services

With

AI, we can perform hyper-personalization in financial services, utilizing

signals from transaction histories, spending patterns, financial goals, etc.

This makes it possible for financial institutions to make financial product

recommendations investment advice, and tailor financial plans for each user.

Customer needs are predicted as AI-driven models then offer customized

solutions such as customer content banking, personalized savings plans, loan

offers, or retirement strategies to enhance engagement and satisfaction.

Moreover,

AI models can also react swiftly and dynamically to the evolution of financial

behavior to engender more profound customer loyalty. Financial institutions

also use sentiment analysis to better understand the customer’s emotions and

adjust services for more targeted, empathetic customer interactions. Switching

from providing generic offerings to servicing the customer with personalized

financial solutions enhances customer experience, fosters relationships, and

promotes future loyalty.

2.2.

Predictive Analytics for Customer Retention

2.2.1.

AI-Based Churn Prediction Models

Financial

institutions, retention of customers is essential, and AI based churn

prediction models are great means of first identifying customers at risk of

exiting. When an AI system analyzes a transaction history, the service usage

patterns, as well as the customer demographics, it can predict which customers

are more likely to disengage. These models serve as a source of such

observations as suppressed account activity or delayed payments early warning

signs for financial institutions.

Financial

institutions have always known customers will become disengaged, it is only

once customers are at risk that financial institutions can take proactive

steps, such as personalized incentives or tailored services, to reengage.

Suppose, for example, a bank cuts interest rates to the customer who seems to

be most unhappy. In this way, these interventions help reducing churn and

increasing customer satisfaction which in turn leads to long term loyalty.

Moreover, AI models continuously learn from churn instances that have already

occurred and invariably get better at their predictions.

2.2.2.

Sentiment Analysis for Customer Feedback

Sentiment

analysis using AI is another layer to look at customer behavior. Such AI tools

look at how customers talk with them (via surveys, reviews, etc.), see if

customers are satisfied or unhappy, and base their sentiment on that. With

real-time sentiment analysis, financial institutions can understand what the

customers are saying about them, allowing them to react to negative feedback in

a timely manner and capitalize on positive experiences.

By

categorizing feedback as positive, negative, or neutral, AI systems give

institutions the ability to proactively fix problems before they become larger

issues so that a normal customer experience can be achieved. Institutions can

also use sentiment analysis to personalize communication and engagement

strategies, rewarding satisfied customers with what they want or addressing

complaints with what the customer wants. More than that, this improves customer

retention as the customer feels heard and valued.

2.3.

Automation in Financial Advisory Services

2.3.1.

Robo-Advisors and AI-Driven Investment Strategies

None

of the applications of AI in financial advisory services are more significant

than Robo-advisors. These AI-powered platforms provide automated financial

planning and investment advisory recommendations that are cheaper than those of

human advisors9-11. Robo advisers use data like

risk tolerance, financial goals and market trends to create customized

investment strategies they fiddle with in real-time as the market's condition.

As

machine learning algorithms are used, the robo-advisors optimize asset

allocation, portfolios, and investment opportunities according to what will

help an individual’s financial objectives. Available with a clean interface,

investment options are available so that those who otherwise could not afford

to use the traditional financial advisor rob advisors democratize access to

financial services. Robo-advisors are expected to get even more powerful and

sophisticated tools like sentiment analysis and alternative data sources to

tweak investment strategies as AI evolves.

2.3.2.

AI-Driven Credit Scoring and Risk Assessment

Machine

learning algorithms are being used also to improve the efficacy of credit

scoring and risk assessment by making the individual’s creditworthiness more

accurate. Historical financial data such as debts and credit history make up

much of how traditional credit scoring models operate, and do so without taking

into account where a borrower may be in terms of their current financial

situation. AI based systems incorporate any of the nontraditional data sources

like transaction history, social behaviour or real time activity of a financial

nature to create an even richer profile of risk.

Using

AI driven systems these systems enhance financial inclusion by providing

underserved population without good history of credit. They also enhance fraud

detection by analyzing patterns and anomalies in real time and flagging

possible fraudulent activities. With AI driven credit models, as customers’

behaviour changes, the credit models can adapt also to make risk assessments

dynamically and accurately, which is essential within the area of financial

risk control as well as guaranteeing regulatory compliance.

3. AI in

Financial Cybersecurity

Cyber

threats have become increasingly rampant with the increase in digital financial

transactions. New vulnerabilities have been created due to the rapid growth of

online banking, mobile payments, and digital financial services that

cybercriminals are looking to exploit10-14. To secure customer data,

protect against fraud, and meet regulatory compliance standards, financial

institutions must embrace advanced security measures. In recent years, AI has

become indispensable in deploying cybersecurity, offering real-time threat

detection, fraud prevention, and automated risk mitigation.

3.1.

Threats in the Digital Banking Landscape

3.1.1.

Cyber Threats in Financial Services

Financial

data and transactions are of high value, and the financial sector is,

therefore, a prime target for cybercriminals. Cyber threats prevalent in

digital banking can be classified as follows:

·Cybercrime: Those who commit this

act do so due to many security weaknesses such as unauthorized transactions,

identity theft and money laundering. Existing rule-based fraud detection

systems are unable to match the rate of evolving fraud techniques.

·Phishing Attacks: These attackers send

deceptive emails, messages, or bogus websites to worm sensitive information

from the user, such as login credentials or credit card details. Attacks in

financial fraud, specifically phishing, are among the most common.

·Malicious software: encrypts a financial

institution's data and asks for ransom payments to regain access. Banking

operations can be crippled, and there is the risk of significant financial and

reputational damage.

·Insider Threats: Employees or

contractors with access to financial systems who may intentionally or

unintentionally expose the data, thus resulting in a security breach, are

termed insider threats. It is possible for AI to watch employee activities

remotely and detect any anomalies that might argue about insider threats.

·Account Takeover Attacks: Cybercriminals

take over a user’s account in a banking institution and generate fraudulent

transactions such as stealing identity.

3.1.2.

AI in Fraud Detection and Prevention

Real-time

fraud detection and adaptive security mechanisms are AI's forte, and they play

a main role in helping the financial sector strengthen its cybersecurity. The

current method of traditional fraud detection relies on rule-based systems,

which are having trouble identifying new threats. However, unlike human-driven

fraud prevention, AI-implemented fraud prevention employs a machine-learning

algorithm to analyze massive data, detect anomalies, and predict fraudulent

activities ahead of time.

·Real-Time Fraud Detection: AI systems

scan through millions of transactions per second to detect suspicious patterns

associated with fraud. These systems flag potentially fraudulent activities

based on transaction amount, transaction frequency, location, and device used.

Unlike other fraud detection models, AI keeps learning from new fraud patterns

daily and becomes better at detecting them.

·Behavioral Biometrics and Anomaly Detection: Security is

improved by determining whether there has been a breach of sanctioned

characteristics of a user in their progress, such as the speed of where a user

typed, where they moved their mouse, and how they generally logged in. The

system can ask for extra authentication or shut down some activity if an

account behaves unusually: those logins from distant, unfamiliar locations,

this sudden gift of lots of money.

·AI-Driven Phishing Detection: AI systems

with content analysis, URL and metadata analysis capabilities are used to

detect phishing attempts. These models take NLP and image recognition to create

models for actually detecting fake login pages, anti-impersonation and

suspicious email patterns. In the area of phishing scams, financial

institutions deploy AI-powered email filters and website monitoring tools to

prevent themselves from being scammed.

·Risk-Based Authentication: AI brings

in security by introducing risk-based authentication (RBA), where the security

implemented on a user depends on his or her risk profile. For instance, a

low-risk user may log in using just a password, while a very high-risk attempt

(such as from an unknown device) may trigger Multi-Factor Authentication (MFA)

or further user verifications.

3.2.

AI-Powered Fraud Detection Systems

Financial

institutions prioritise fraud detection as a high priority as cybercriminals

get smarter. Normally, traditional fraud detection systems rely on predefined

rules and patterns and are, thus, limited in their ability to detect the

emergence of novel and sophisticated fraud strategies. However, with machine

learning, anomaly detection, and behavioral biometrics, AI-based fraud

detection systems have the ability to deliver dynamic and real-time solutions.

For

instance, Machine learning models are trained on huge chunks of the transaction

data, which on the basis of which the model learns what are the pattern of

normal and abnormal activities. And especially since they are so effective at

detecting anomalies of the sort (such as high value transactions from strange

locations), which may indicate fraud. AI systems are different from rule-based

systems since they learn from new data, so they are more accurate in

identifying attempts of fraud without increasing the number of false positives.

One

other powerful tool used in AI driven fraud detection is behavioral biometrics.

That is focused on analyzing the user’s own unique pattern of interacting with

such devices with, say: typing speed, mouse movements, etc. The system can flag

an unusual action such as logging in from a strange location or running an

unusual transaction. At the same time that is does this, it also prevents

identity theft and account takeovers, while keeping user experience intact.

Together,

these AI driven systems enable the financial institutions to detect the frauds

in real time, thus minimizing the losses to the financial institutions as well

as to minimize the customer trust by keeping the customers busy within their

‘legitimate’ activities. AI’s ability to learn and adapt lends itself to be a

valuable tool in dealing with financial cybersecurity as it grows.

3.3.

AI in Regulatory Compliance and Risk Management

Financial

risk mitigation using regulatory compliance for suppressing money laundering,

fraud and other financial crimes. They will have stringent monitoring and

reporting obligation of financial transactions as per regulations such as KYC

(Know Your Customer), AML (Anti Money Laundering) and GDPR (General Data

Protection Regulation). In most cases, compliance processes involve high

volumes and complexity of data largely leaving financial institutions prone to

make mistakes alongside inefficiency. In fact, AI is automating these areas by

means of automation and real time data analysis, and then through predictive

modeling.

AI

powered solutions make the KYC and AML processes more usable through the

automata of identity verification, watching transactions for malpractices

activities, and risk profiling assessment. AI for KYC help with advanced

artificial intelligence recognition and document scan technology to carry on

the identification of customers with the least human involvement to cut down on

the onboarding time and make the data way more precise. Continuous monitoring

is also available to financial institutions so that they can have the ability

to keep their customer profiles current with real time behaviour as opposed to

periodic reviews. AI takes advantage of machine learning to apply the analysis

of transaction data in detecting hidden patterns of money laundering activities

in money transfers or crossborder transactions for AML.

As

for regulatory technology (RegTech), the use of AI is also prominent in the

sense that it automates the analysis of legal and regulatory texts. Natural

language processing (NLP) tools allow financial institutions methods to read

complex documents without interpreting them manually, helping financial

institutions stay updated about the changes in the regulations. Additionally,

AI fueled predictive models can foresee considerable risk before they become

real, helping financial institutions to act on compliance risk competently

thereby eliminating penalties.

In

aggregate, AI is reimagining the fundamentals of what financial institutions

can do in terms of regulatory compliance and risk management as more efficient,

accurate and scaled. Similarly, AI is set to assume an increasingly important

role in ensuring compliance in increasingly complex regulatory environments,

allowing firms to calibrate and maneuver around regulatory challenges while

ensuring security and maintaining trust in customers.

4. AI-Driven

Banking Ecosystems

The

revolution of AI facilitates automation, financial forecasting, and data-driven

decision-making in banking ecosystems. Banks are moving to digital-first models

as AI-driven technologies streamline operations, enhance customer experience,

and encourage innovation through open banking frameworks. The combination of

leveraging AI through API15

banks can leverage driven financial systems to provide more personalized, more

efficient and safer services.

Figure

1.

AI-Driven Banking Ecosystem Framework

The

core components for leveraging AI in financial services allow this to inform

the creation of AI banks of the future. It identifies 4 main objectives that

converge to a goal: profitability, omnichannel experience, personalization at

scale, speed, and innovation. These are the goals of AI in making financial

institutions change how they relate with customers, within operational

efficiency, and in all-around decision-making at the centers. It breaks down

AI-driven banking into many layers that address the important aspects of modern

financial services.

The

operating model and core technology, which are at the foundation of this

framework, are the backbone for AI-driven transformation. A technical thruway

in this layer draws attention to the critical role a tech-forward approach

would play in combining AI with data management, modern API architecture,

leveraging cybersecurity controls, and intelligent infrastructure. The

operational efficiency of banking institutions is further strengthened by

AI-powered automation and cloud-based solutions. Moreover, the model helps to

enable agile working, if not promote it, remote collaboration and

transformation through hiring and reskilling strategies.

The

framework moves toward AI-powered decision-making, where advanced analytics and

AI capabilities are important. Businesses deploy AI-driven tools like natural

language processing, computer vision, facial recognition, and robotics to

improve customer acquisition, credit evaluation, fraud detection, collections

and personalized recommendations. Using these technologies enables banks to

foresee customer needs and automate real-time risk assessments and systems for

fighting fraud.

At

the top level, the framework looks into more intelligent banking solutions to

restructure customer engagement. This involves targeted financial services,

smart financial channels and uncomplicated customer experiences across multiple

channels, including mobiles, smart banking devices, partner ecosystems, etc.

Digital marketing using AI-driven analytics, automated customer service

support, and cross-selling strategies helps banks provide hyper-personalized

financial experience without losing operational efficiency.

Ultimately,

helping customers thrive in a bank efficiently in today’s uncertain world,

which relies on technology to overcome and adapt to global norms, and also

build a bank with a holistic technology-first approach to improve customer’s

experience and second to secure its bank in cybersecurity and compliance and

sound decision making. By implementing AI at multiple levels, financial

institutions can initiate sustainable growth, optimize resources and achieve

high profitability with an acceptable level of competition in the evolving

digital banking environment.

4.1.

Smart Banking and Automation

4.1.1.

AI-Powered Process Automation in Banks

Loan

approvals, customer service, risk assessment, and any kind of compliance check

have always been manual processes done by banks16-19.AI

is transforming these operations thanks to process automation incorporating AI,

which lowers costs and improves efficiency. When RPA and AI are used together,

banks can make routine work, like verification of documents, transaction

processing and fraud detection, a thing of the past.

Customer

service was one of the key areas where AI-driven automation is in action. These

virtual assistants and AI-powered chatbots enable all-time customer support by

answering inquiries, making transactions and resolving any issue without human

intervention. Natural Language Processing (NLP) and machine learning help these

virtual assistants understand the customer’s query and responds to them better

and better.

AI

also helps in automating underwriting process in case of loans and credit

approvals. Whereas traditional loan approval methods and systems are based on

clearly defined criteria, the AI assisted loans models utilise a variety of

data, including current real time financial behaviour, transaction history and

alternative sources of creditworthiness. The resulting bias reduction,

accelerated approvals, and expanded credit access to underserved populations

all add up to improving peoples’ access to credit.

AI

powered automation is another major application of automation in banks that

deal with regulatory compliance as well. AI driven tools take hygiene of your

data to a whole new level as they analyse really massive dataset to uncover any

suspicious activity from AML like as well as Know Your Customer (KYC). But

these systems reduce human exposure to error and in turn promote greater

accuracy in compliance reports for avoiding bank regulatory penalties.

4.1.2.

AI-Driven Financial Forecasting

In

banking, financial forecasting is crucial in assisting institutions in

anticipating what will happen on the market, the behavior of customers, etc.

Using AI powered predictive analytics, these models analyse historical data,

macroeconomic indicators as well as real time financial transactions to create

extremely predicated forecasts. Such as, AI based forecasting tools assist in

predicting loan defaults, figuring out investment chances, along with liquidity

administration. They are continuously learning from new data and are improving

their predictions and decreasing financial risk. Banks can also use AI to

detect early signs of economic downturns as they use global financial patterns,

interest rates, consumer spending behavior, etc. to detect the early signs of

this and take proactive measures.

Moreover,

AI derived sentiment analysis allows banks to understand market sentiment from

analyzing news articles, social media trends, users’ feedback. Sentiment driven

insights can help banks better understand risks and make more informed

investment decisions by integrating the sentiment driven insights with the

financial forecasting. Beyond risk management, AI driven financial forecasting

also helps in customer’s personalized financial planning. AI helps banks

recommend tailored financial solutions based on individual spending habits,

saving goals and investment preferences. It helps bank in customer engagement

and loyalty resulting in longer lasting relationships between the bank and its

clients.

4.2.

AI and Open Banking

4.2.1.

Role of AI in API-Driven Banking Ecosystems

The

financial industry is being changed by open banking that allows third-party

providers to access banking data via Application Programming Interfaces (APIs).

Open banking has a huge role played by AI in financial data analysis, making it

more secure and allowing for scalable personal financial services.

Automated

financial management is one of the main advantages of AI in API-driven banking.

AI tools aggregate the data from a number of banks, as well as other financial

institutions, through which you get a single window or view of your finances.

AI-driven budgeting assistants let customers keep an eye on expenses, save more

money and receive real-time financial insights.

Open

banking ecosystems are additionally secured by AI that detects anomalies in API

interactions. Third-party applications work according to the defined security

standard. Machine learning algorithms are run on transaction patterns and

analysed to detect fraudulent activities. AI-based identity verification

systems also secure authentication processes by reducing the risk of

unauthorized access.

Additionally,

chatbots enabled through open banking platforms are powered by AI for easy and

smooth customer interaction. Built on chatbots, these financial advice chatbots

are automated payments so that one chatbot can handle payments from one

financial institution to another and can be used to handle all financial

transactions across various financial institutions.

4.2.2.

AI-Powered Data Analytics for Financial Decision-Making

The

openness of banking generates loads of data, a great vibe that AI can leverage

to help make smarter financial decisions. The use of predictive analytics using

next-gen and AI leads banks and financial institutions to get deeper insights

into the behavior of their customers, credit risks, and the investment trends

taking place, such as how a customer's spending history can give AI the means

to tailor financial products like loan offers, dynamic interest rates or

recommendations on how to invest. Personalization to this level boosts customer

satisfaction and makes financial inclusion more possible. AI's help to banks in

assessing the creditworthiness of individuals and businesses by alternative

data sources continues to be risk assessment models powered by AI that can

evaluate the individuals and businesses ' creditworthiness based on transaction

history, bill payment, and digital footprint, among others. In this approach,

banks can lend to customers without a proper traditional credit history that

has shown responsible financial behavior. Similarly, AI-driven data analytics

helps enhance corporate banking by giving real-time insights into cash flow

management, debt forecasting, and investment optimization. Financial models

powered by AI achieve revenue forecasting, cost-saving identification, and the

automation of financial plans for businesses.

Furthermore,

in the open banking space, AI helps regulate compliance by analyzing the

transactional data to detect money laundering, fraud, and tax evasion. With

AI-driving RegTech solutions, financial institutions can ensure compliance with

changing regulations is met, and the cumbersome work that often comes with

manual audits and reporting can be tamed.

Table

1.

AI Applications in Open Banking

|

AI

Application |

Functionality |

Impact

on Open Banking |

|

Automated

Financial Management |

Aggregates

data from multiple accounts and provides real-time insights |

Enhances

financial planning and transparency |

|

AI-Powered

Security & Fraud Detection |

Monitors

API interactions for anomalies and unauthorized access |

Strengthens

security and prevents financial fraud |

|

Predictive

Analytics for Credit Scoring |

Assesses

creditworthiness using alternative financial data |

Expands

access to credit for underserved populations |

|

AI-Driven

Investment Recommendations |

Analyzes

spending habits and market trends to provide investment insights |

Enables

personalized financial decision-making |

4.3.

The Impact of AI on Traditional vs. Digital Banks

Artificial

Intelligence (AI) is transforming the banking industry from conventional banks

to digital ones, also known as neobanks. Moving forward, AI is a core piece of

neobanks, and traditional banks will adopt it to keep up with the pace20-24. AI plays different roles in these

banking models and dictates how they run, interact with the customer, and

manage risk.

4.3.1.

AI-Driven Innovation in Neobanks

Digital

or neuro banks don’t have physical branches; they operate through technology to

provide banking services. However, their business is based on AI, with AI being

the main driver, making it possible to provide hyper-personalized financial

services, real-time decision-making, and cost-efficient operations.

AI-powered

customer service is one of the major releases in neobanks, having chatbots and

virtual assistants. These AI-based systems make customer inquiries,

transactions, and financial advice without human intervention. Unlike

traditional banks, the neobanks intelligently combine AI to have a unified

channel, working on mobile apps and web platforms, making the entire banking

experience seamless and 24/7. Personalized financial management also picks up

in neobanks with the help of AI. AI analytics then monitors users’ spending

habits, classifies their transactions, and offers highly personalized insights

into budgeting, savings and investment opportunities. Many neobanks integrate

AI-powered recommendation engines that provide the best financial products according

to an individual's financial behaviour to fulfill their mission.

The

biggest advantage of AI in the realm of neobanks is that it can perform

automated risk assessment and lending decisions. In particular, traditional

banks typically consider credit scores and hand assessments to determine

loanability. However, NEOBANKS use AI driven credit scoring models that do not

base their scoring on just the history of payments, but also on social

behavior, the history of transaction, spending patterns in real time. That

means the neobanks are able to lend to people who don’t have traditional

credit, for instance gig workers and freelancers.

Fraud

and cybersecurity are of paramount importance in the neobanks: they are AI

driven. Transactions are monitored by these machine learning models in real

time, finding suspicious activities long before they can be done. Other types

of biometrics, such as behavioral biometrics (keystroke patterns, device

recognition) continue the security path by detecting any attempts of

unauthorized access.

Table

2.

AI Applications in Neobanks

|

AI

Application in Neobanks |

Functionality |

Impact |

|

AI-Powered

Chatbots |

Automated

customer support and financial assistance |

24/7

seamless banking experience |

|

Personalized

Financial Insights |

AI-driven

budgeting, spending analysis, and investment suggestions |

Improved

customer engagement and financial literacy |

|

AI-Based

Credit Scoring |

Alternative

data-based risk assessment |

Expanded

credit access for underserved individuals |

|

AI-Driven

Fraud Detection |

Machine

learning models for anomaly detection |

Enhanced

security and fraud prevention |

4.3.2.

AI Adoption in Traditional Banking Institutions

Traditional

banks have a pretty satisfactory base of the infrastructure but they lag in

digital transformation as they have an old system of the legacy tied to the

regulatory bound and the complex operative structure. While the rate of

adoption of AI in traditional banks is being sped up as they look to become

more efficient, better service their customers, and maintain their relevance to

the digital first challengers.

Process

automation is one of the key areas on which the traditional banks are using AI.

Manual banking tasks like verifying a document, approving a loan and producing

a compliance report are being automated using AI Powered Robotic Process

Automation (RPA). Faster processing speed as well as lowering the operational

costs helps traditional banks fight off neobanks in winning the race for

efficiency.

AI

powered predictive analytics is also integrating into traditional banks to be

used in risk management and also investment strategies. The machine learning

models are to predict Loan Defaults, Market Fluctuations, and Customer Churn

with analysis of historical data. Using AI driven insights, the banks run on

traditional are able to provide better and more competitive loan products,

better road to manage the asset, better road to diversify the portfolio.

The

area of AI adoption in traditional banking also involves realizing more

personalized customer engagement. Banks can serve customers with financial

products tailored to the customer's behaviour using AI-driven recommendation

engines. Whereas neo banks by nature are digital-first, when traditional banks

implement AI tools, it is for hybrids, which involve combining mobile banking

with traditional platforms with in-branch AI services. Traditional banks also

take the mantle of fraud prevention and cyber security issuances by building

AI-powered transaction monitoring systems. Unlike rule-based fraud detection

methods based on static rules, AI models analyse real-time transactional,

device behaviour and geolocational patterns to uncover data related to fraudulent

activity. Combining biometric authentication (face recognition, fingerprint

scanning) with AI-based risk analysis, traditional banks protect security

without irritating the client.

Table

3.

AI Integration in Neobanks vs. Traditional Banks

|

AI

Integration |

Neobanks |

Traditional

Banks |

|

Customer

Service |

AI-driven

chatbots and virtual assistants |

AI-enhanced

support alongside human agents |

|

Financial

Management |

AI-powered

budgeting and financial insights |

Personalized

financial planning tools |

|

Lending

& Credit Scoring |

AI-based

alternative credit assessments |

AI-assisted

traditional credit evaluations |

|

Fraud

Detection |

Machine

learning models for real-time anomaly detection |

AI-powered

transaction monitoring with biometric authentication |

4.4.

AI-Powered Decision Making

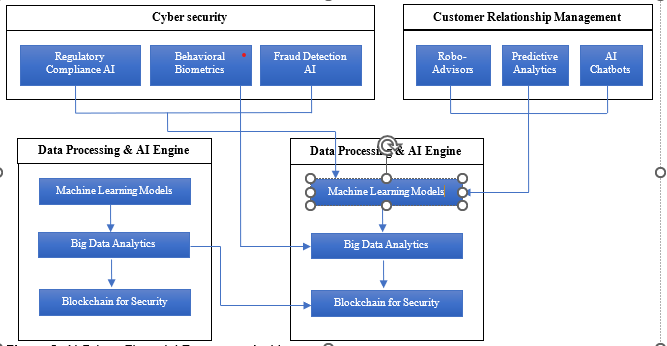

Figure

2.

AI-Driven Financial Ecosystem Architecture

A

high-level architecture for an AID-driven financial ecosystem and how the

components of cybersecurity, customer relationship management (CRM), banking

ecosystem, etc., interact. The backbone of this framework is a data processing

AI engine that powers different types of AI-powered capabilities through

machine learning models, data science, and blockchain security. It offers these

elements by providing automation, predictive analytics, and secure transactions

within this financial industry. The cybersecurity module consists of AI-based

fraud detection, regulatory compliance, and behavioral biometrics to improve

security against financial threats.

The

CRM module is on the customer-facing side and uses AI-based chatbots,

robo-advisors, and predictive analytics to enhance engagement and customer

decision-making. Smart banking and open banking APIs with banking AI financial

forecasting perfectly integrate the banking ecosystem and digital banking

experiences. This demonstrates the nature of interconnectedness of

these/components together and how AI-driven technologies help personalize, be

secure, and run efficient operations within modern financial institutes,

forming the emergence of AI banks.

5.

Challenges and Ethical Considerations in AI-Driven Finance

Artificial

intelligence (AI) is transforming the financial sector, but so are its

associated challenges and ethics. From a data privacy perspective, a financial

institution25-27 regulator, or

consumer must control the data they collect, process and monetize. While AI

boosts efficiency, decision-making, and customer experience, fairness in using

AI for financial decision-making, transparency of AI usage, and building trust

in AI-driven financial ecosystems must be resolved.

5.1.

Data Privacy and Ethical Concerns

As

AI increasingly integrates into finance, it means collecting and analyzing

sensitive customer data, including transaction history, personal identity

information, and financial behaviors. AI-driven insights that strengthen

financial services also involve serious data privacy and ethical issues

concerning security, consent, and transparency.

Cybercriminals

target financial institutions due to highly lucrative prospects in the

exploitation of vulnerabilities in AI powered systems. As the AI driven banking

becomes more and more popular, therefore, cyberattacks like data breaches,

phishing, and ransomware become more and easier to perform. You need to ensure

that you are keeping your AI models protected from cyber threats so as to

ensure the security of the customer’s data.

Also,

there is the customer consent and transparency issue. However, as black boxes,

many of the AI systems can be explained to customers or regulators. Such

practice raises issues about how customer data is used and shared, as well as

monetized. The fact that AI algorithms constantly process customer data,

without adequate disclosure, makes it possible that such data will be misused

or exploited without the knowledge of the customers. Like any other financial

institution, they also have to abide by the stringent data protection

regulations, which include, the General Data Protection Regulation (GDPR) in

Europe and the California Consumer Privacy Act. Translated into regulations,

this means that financial institutions must be transparent and get consent from

the customers for the way their personal data is being processed and users must

have control over their personal information.

5.2.

Bias in AI-Driven Financial Decision-Making

The

financial systems are AI-driven to help decision-making on lending, credit

scoring, fraud detection and investment management. Despite that, AI models are

vulnerable to bias, and the consequences can be unfair, discriminatory outcomes

for minority or underrepresented groups.

One

of the major contributors to bias in AI finance is biased training data.

Historical data will inform the AI models, and if past financial decisions were

affected by discriminatory practices, AI systems will be imbued with the same

biases. The above is just an example of the risk. Suppose the AI-based credit

scoring system is trained using data that favors the high-income candidate from

certain demographics. In that case, it will be biased disproportionately in

rejecting loan applications from the minority or low-income group.

This

also creates an algorithmic bias in automated decision-making. Gender, race,

age, or location may be taken into account in subtle ways by AI models that

they have no wish to discriminate, and it will be hard to navigate around the

implicit bias embedded in machine learning. For example, biased mortgage

approval algorithms can result in disparities in getting home loans and fewer

financial inclusions in these disadvantaged communities.

The

impact of AI bias in finance can be severe, leading to:

• Unfair lending decisions in favor of

certain demographics against other demographics.

• Exclusion from financial services for

individuals with limited financial history.

• Regulatory scrutiny and legal actions

against financial institutions for discriminatory practices.

Financial

institutions must take proactive steps to detect, mitigate, and prevent AI bias

through:

• Ensuring fairness in the AI models by

using diverse and representative data for training.

•Addressing the trust issues in

decision-making processes through Explanable AI (XAI).

• Regular catching and testing for

unintentional discrimination using regular AI.

5.3.

Regulatory and Compliance Challenges

Regulatory

constraints for financial institutions are brought to bear in the face of the

rapid adoption of AI in finance. Though regulators around the world are trying

to put AI governance on a stable footing, gaps in legal frameworks in place

create risks for both the banks and customers.

AI

accountability is one of the most important challenges related to regulation.

There is no transparency in many of AI driven financial decisions, and

regulators find it hard to determine who might be liable for such erroneous or

unfair decisions.

Another

issue at hand is the fragmentation of the global regulators. Complying can be

tricky for multinational banks in light of various AI regulations of different

countries. This differs from the risk-based AI governance approach undertaken

by the European Union in its AI Act, while other jurisdictions, such as the

U.S. and China, have their regulatory approaches. Cross-border financial

institutions need to navigate complex compliance requirements.

Moreover,

AI-driven finance must comply with existing financial regulations, such as:

•AI models need to detect fraud

without violating privacy rights while meeting Anti Money Laundering (AML) And

Know Your Customer (KYC)

• AI-driven credit decisions must

ensure fair lending laws, which prevents AI from being discriminatory.

•Consumer protection regulations via

AI are launched in the consumer protection area; they will have to meet certain

transparency conditions in the pricing, disclosure of risks, and investment

strategies.

6. Future

Trends and Research Directions

AI’s

advances in the financial industry are becoming increasingly complex. Several

of these key trends and research directions are expected to be realized in the

future of AI in finance, Decentralized Finance (DeFi), quantum computing, and

emerging technologies that aim to fundamentally repurpose the finance services

industry.

6.1.

AI Advancements in Decentralized Finance (DeFi)

Blockchain

ecosystem's addition of Decentralized Finance (DeFi) is in the realm of

emerging services that provide financial services with no need for any

traditional intermediaries, such as banks or brokers. DeFi works to move to a

financial system with transparency, inclusiveness, and efficiency by using

smart contracts and blockchain technology. DeFi platforms are on their way to

becoming mainstream. As AI serves as an agent of change, it is in a very good

position to make AI a major player in driving the development of the platforms

and solving some of the critical problems: scalability, security and user

experience.

AI-powered

smart contract optimization is one of the major advances in AI in DeFi.

Decentralized networks power smart contracts. Smart contracts are

self-executing agreements on these networks; they are the core of DeFi

protocols. By automating the way the contracts are executed and predicting

issues, CAD can improve smart contract functionality with AI. Machine learning

models in AI learn to find the patterns in smart contract behavior to increase

accuracy and efficiency in contract execution and minimize error and

exploitation.

AI

can be applied in liquidity management to analyze massive amounts of market

data and envision liquidity shortages or bottlenecks occurring in DeFi

protocols. A decentralized exchange that leverages AI-driven predictive

analytics can make the Automated Market Maker (AMM) model as efficient as

possible to ensure better price stability and liquidity, which are the very

characteristics that can trip up many DeFi ecosystems as being inherently

skewed towards volatility.

DeFi

is also seeing its share of AI bubble security. Such vulnerabilities in the

DeFi protocols have given rise to smart contract hacking and other activities.

Now, with AI-powered systems, deploying them to fill a blank for real-time

monitoring and analysis of blockchain activity to look for suspicious behaviors

is possible. Machine learning models can catch anomalies in transaction

patterns and alert for a potential case of fraud or hacking beforehand. This is

extremely important for DeFi pools to grow and become a trusted and secure

presence in a highly decentralized environment.

6.2.

AI’s Role in Quantum Computing for Finance

Quantum

computing is a paradigm change in computational power, capable of solving

problems beyond the reach of classical computers. Although nascent quantum

computing is in its infancy, when combined with AI, its applications can be

found in areas of optimization, risk management and financial modelling,

towards a market adaptation that promises a revolution in the finance sector.

Portfolio

optimization is one of the most exciting portfolio applications of quantum

computing. Large-scale and complex portfolios easily overwhelm traditional

optimization techniques due to the large number of variables. Solving problems

of optimization using quantum algorithms, such as quantum annealing and

variation quantum algorithms, can be done very quickly, a fraction of the time

it would take by classical methods. By utilizing quantum computing and AI,

financial institutions can design real-time, dynamic inventory strategies

considering a wider spectrum of variables and market conditions. Such a

strategy could yield better returns and improved portfolio risk-adjusted

performance.

Quantum

computing teamed up with AI could transform risk management with the power to

more accurately model and predict complex financial eventualities. Can quantum

algorithms fasten Monte Carlo simulations that are usually deployed to assess

risk by spectator thousands of virtual market scenarios? Quantum-enhanced

simulations could enable much faster and more accurate risk simulation that

could be used by financial institutions to better make decisions in the face of

uncertainty.

AI-driven

quantum computing will also be used for cryptographic security. With most, if

not all, the encryption algorithms used to protect the flow of money today, any

luck of the draw that a quantum computer breaks one of them is good luck.

However, quantum-enhanced AI might be able to help develop new cryptographic

techniques, like post-quantum cryptography, that will stand up to quantum

computing attacks. This will be important as financial systems increasingly

need to guard against quantum machines with computational power.

6.3.

Emerging AI-Powered Financial Innovations

A

host of innovative financial technologies are now being developed thanks to AI

and are likely to define the future of finance. Many of these new AI-powered

innovations are improving the customer experience, making smarter financial

decisions, and providing a more personalized financial experience.

Among

the innovations to appear are AI personal finance management tools. Machine

Learning And Natural Language Processing (NLP) power these platforms, which

offer tailored financial advice, budget tracking, and savings recommendations.

Personal finance assistants based on AI bring in users to spend, save, and

invest intelligently according to their financial goals. These tools give you

traditional financial advice and, if you need it, based on an individual's

spending patterns and economic time.

Furthermore,

AI is used in behavioral finance, studying how psychology affects financial

decision-making. Sentiment analysis tools that use AI are employed to analyze

public sentiment, news, and social media trends and answer whether the markets

will go up, down, or somewhere in between. The financial sector is using AI to

discover consumer behavior. It can then use that to tailor marketing approaches

and develop new products that fulfill the customers' needs.

AI-enhanced

digital banking is another emerging innovation. Banks use AI to enable seamless

and frictionless experiences with everything from personalized digital wallets

to robo-advisors. Natural language command-powered voice-activated banking

services are gaining momentum, and customers can perform banking tasks using

the commands. AI is also powering payment systems, with AI-driven payment

systems offering higher levels of security and speed through technologies like

biometric authentication and blockchain-based payment rails.

7.

Conclusion

Artificial

Intelligence (AI) is transforming the financial industry by creating the path

for more efficient and competent operations, better customer experience, and,

ultimately, innovation. The areas of application of AI in Customer Relationship

Management (CRM), security services, and the banking ecosystem are in their

ways of development, which provide financial institutions with opportunities to

continue to be competitive and meet the needs of the ever-increasing consumer

demand. Financial services increasingly rely on AI to achieve better returns,

eliminate waste and errors, improve customer retention, detect fraudulent

behavior and manage risks.

The

rapid adoption of AI in finance presents several challenges, such as data

privacy concerns, bias in decision-making, regulatory compliance, etc. If

financial institutions are to follow the trend of integrating AI, addressing

the above challenges via ethical guidelines, transparent AI practices, and

sound regulatory frameworks will be the day's need to ensure AI's positive

contribution to the financial ecosystem. However, the future of AI in finance

seems promising. It should further advance with decentralized finance (DeFi),

quantum computing and more emerging AI-powered innovations, bringing new and

unique value to the financial services delivery market. As AI research

continues, develops, and collaborates, the role of AI in the next generation of

financial technologies will continue to grow centrally.

6.

References

- Birch DG,

Rutter K. Where are the customers’ bots? The AI paradigm shift in retail

banking. Journal of Digital Banking 2023;8:132-140.

- Kangra

K. A Paradigm Shift. Artificial Intelligence Technology in Healthcare: Security

and Privacy Issues 2024;1.

- Nadella

GS, Gonaygunta H. Enhancing Cybersecurity with Artificial Intelligence:

Predictive Techniques and Challenges in the Age of IoT. International Journal

of Science and Engineering Applications 2024;13:30-33.

- Roshanaei

M, Khan MR, Sylvester NN. Enhancing cybersecurity through AI and ML:

Strategies, challenges, and future directions. Journal of Information Security

2024;15:320-339.

- Vegesna VV.

Enhancing Cybersecurity Through AI-Powered Solutions: A Comprehensive Research

Analysis. International Meridian Journal, 2023;5:1-8.

- Jonas D, Yusuf NA,

Zahra ARA. Enhancing security frameworks with artificial intelligence in

cybersecurity. International Transactions on Education Technology 2023;2:83-91.

- Akhtar

ZB, Rawol AT. Enhancing Cybersecurity through AI-Powered Security Mechanisms.

IT Journal Research and Development 2024;9:50-67.

- Adewusi

AO, Chiekezie NR, Eyo-Udo NL. The role of AI in enhancing cybersecurity for

smart farms. World Journal of Advanced Research and Reviews 2022;15:501-512.

- Li

F, Xu G. AI-driven customer relationship management for sustainable enterprise

performance. Sustainable Energy Technologies and Assessments 2022;52:102103.

- Galitsky

B. Artificial intelligence for customer relationship management. Springer

International Publishing, Cham 2020.

- Shaik

IAK, Mohanasundaram T, KM R, Palande SA, Drave VA. An Impact of Artificial

Intelligence on customer relationship management (CRM) in the retail banking

sector. European Chemical Bulletin 2023;12:470-478.

- Daqar

MAA, Smoudy AK. The role of artificial intelligence in enhancing customer

experience. International Review of Management and Marketin 2019;9:22.

- Ameen

N, Tarhini A, Reppel A, Anand A. Customer experiences in the age of artificial

intelligence. Computers in human behavior 2021;114:106548.

- Flaherty

B, Heavin C. Positioning predictive analytics for customer retention. Journal

of Decision Systems, 2015;24:3-18.

- Building

the AI bank of the future, McKinsey & company.

- Jung

D, Dorner V, Glaser F, Morana S. Robo-advisory: digitalization and automation

of financial advisory. Business & Information Systems Engineering

2018;60:81-86.

- George AS.

Robo-Revolution: Exploring the Rise of Automated Financial Advising Systems and

Their Impacts on Management Practices. Partners Universal Multidisciplinary

Research Journal 2024;1:1-16.

- Batchu RK. Artificial

Intelligence in Credit Risk Assessment: Enhancing Accuracy and Efficiency.

International Transactions in Artificial Intelligence 2023;7:1-24.

- Mishra S. Exploring the impact

of AI-based cyber security financial sector management. Applied Sciences

2023;13:5875.

- Udeh

EO, Amajuoyi P, Adeusi KB, Scott AO. The integration of artificial intelligence

in cybersecurity measures for sustainable finance platforms: An analysis.

Computer Science & IT Research Journal 2024;5:1221-1246.

- Thapaliya S.

Examining the Influence of AI-Driven Cybersecurity in Financial Sector

Management. The Batuk 2024;10:129-144.

- Bao Y,

Hilary G, Ke B. Artificial intelligence and fraud detection. Innovative

Technology at the Interface of Finance and Operations 2022;I:223-247.

- Kumar

N, Agarwal P, Gupta G, Tiwari S, Tripathi P. AI-Driven financial forecasting:

the power of soft computing. In Intelligent Optimization Techniques for

Business Analytics 2024;146-170.

- Agarwal

A, Singhal C, Thomas R. AI-powered decision-making for the bank of the future.

McKinsey & Company 2021.

- Lazo

M, Ebardo R. Artificial intelligence adoption in the banking industry: Current

state and future prospect. Journal of Innovation Management 2023;11:54-74.

- Basly

S. Artificial Intelligence and the Future of Decentralized Finance. In

Decentralized Finance: The Impact of Blockchain-Based Financial Innovations on

Entrepreneurship (pp. 175-183). Cham: Springer International Publishing 2024.

- Iyer R, Bakshi A. Artificial Intelligence and Quantum Computing Techniques for Stock Market Predictions. Deep Learning Tools for Predicting Stock Market Movements 2024;123-146.