The Impact of Autonomous Vehicles on P&C Insurance: Preparing for the Next Frontier of Risk and Liability

Abstract

The arrival of autonomous vehicles

(AVs) promises to revolutionize transportation with significant implications in

the property and casualty (P&C) insurance business. Traditional paradigms

for risk assessment and liability in auto insurance are under attack as

self-driving technology evolves. This paper examines the emerging risks and

opportunities that AVs have introduced to the P&C insurance world. On the

key considerations side, product and manufacturer liability for human operator

injuries, the increase in automation of insurance underwriting using advanced

technologies like AI and machine learning and potentially decreased accident

frequency but an increased severity in accidents caused by more advanced

vehicle systems is all on the table. The paper also considers regulatory

frameworks that guide the adoption of AV and their implications for Insurance

should the different modes of operation of AV and human-driven vehicles begin

to converge. It addresses how telematics and data analytics play into a fault

and pricing premium decision in a market where AVs are dominant. The paper discusses

adapting to the evolving risk environment and looks at regional Collaboration

between insurers, policymakers and automakers. Insurers can prepare for the

future in which AVs rewrite mobility, assure against uncertainty and capture

opportunity in the era of transformational change through understanding these

dynamics. The alarming findings add weight to the call to proactively develop

insurance products and other risk management apparatuses to fit into the

complexities of autonomous technologies.

Keywords: Autonomous vehicles,

Property and casualty, Risk assessment, Telematics, Regulatory frameworks

1.

Introduction

1.1. The rise of autonomous vehicles

One of

the 21st century's most transformative innovations is autonomous vehicles

(AVs). AVs are aggressively approaching widespread adoption via leveraging

advanced technologies such as artificial intelligence (AI), machine learning

and sensor integration1-3. Their

potential benefits encompass improving road safety, decreasing traffic

congestion and many others. However, their adoption also brings a new frontier

of challenges, particularly for industries like property and casualty (P&C)

insurance, whose risk and liability paradigms are rooted in how humans behave.

1.2. Disrupting traditional insurance models

Traditionally,

this builds on determining how drivers behave, how frequently accidents occur

and how much damage is incurred per accident. However, with AVs, human error

(one of the principal causes of accidents) is eliminated and the spotlight

shifts to software dependability, sensor performance and cyber vulnerabilities.

This shift raises critical questions: In an AV accident, who is liable: the

manufacturer, the software developer or the vehicle owner? Such changes,

however, require rethinking risk assessment, underwriting treatment and premium

structures.

1.3. Regulatory and technological challenges

AVs'

regulatory environment is still evolving, as there are still many differences

in the standards between jurisdictions. They determine how insurers consider

liability and coverage themselves. Integrating telematics, real-time data

analytics and AI tools creates a new complexity in fault determination and

pricing premiums. Connected vehicles could be vulnerable to hacking,

complicating insurers' profiles even more.

1.4. Preparing for the next frontier

AVs are a

challenge and an opportunity for the P&C insurance industry. Insurers must

get used to it in an ecosystem where technology-driven risks and liabilities

replace the traditional metrics. However, insurers, automakers, regulators and

tech developers must work together to traverse this transition successfully.

This paper aims to understand these dynamics and learn some lessons for the

insurance industry to prepare the insurance sector for the widespread adoption

of AVs and embrace the next frontier of mobility.

2.

Autonomous Vehicles: Evolution and Technology

The story

of autonomous vehicles has gradually changed, but it is a transformational

story fuelled by technology and efforts to achieve safer, more efficient

transportation systems. -based on understanding the evolution and technological

foundation supporting AVs4-7, we can

project their impact on industries like property and casualty (P&C)

insurance.

2.1. Levels of vehicle automation

The six

SAE levels of automation are from level 0 (no automation) to level 5 (full

automation). They represent the industry standard of the level of automation in

a vehicle, which has governed discussions around advancing technologies,

regulatory frameworks and insurance implications.

Figure 1: SAE Automation Levels for Autonomous

Vehicles.

· Level 0: The human driver takes

over driving tasks individually, as and when needed. Currently, automobiles in

this category comprise a large part of the market, for which risk is attributed

only to human error and traditional underwriting insurance models prevail. This

stage has historically been the basis for actuarial calculations and liability

frameworks in the insurance industry.

· Level 1: Features Vehicles at

this level offer things like adaptive cruise control or lane-keeping assistance

and driver assistance. Automation only reduces to specific tasks, causing the

driver to remain fully engaged. From an insurance point of view, although minor

changes in underwriting models, liability remains where it has been on the

driver.

· Level 2: Combines steering and

acceleration control, with the driver monitoring the environment, intervening

as required hardware and Partial Automation. With the advent of Level 2

vehicles, the distinction between driver and system responsibility becomes

increasingly vague and thus, insurers must think about dual fault scenarios.

This phase lays a foundation for hybrid liability frameworks.

· Level 3: Level 3 Automation.

This level of automation allows the vehicle to perform most driving tasks, but

the driver must always allow the vehicle to intervene when conditions warrant

it. That transition point highly impacts insurance models because the liability

shifts more towards the manufacturer or the software provider in case of system

failure. At this stage, regulatory debates intensify and safety standards and

accountability are debated.

· Level 4: High Automation or

Condition-based (e.g. geofenced) - Vehicles at this level can perform all

driving functions under specific conditions. However, human intervention is

still allowed. As driver fault continues to fade, the models adapt to changes

in product liability and advanced AI systems. Adjusting software reliability

and environmental constraints are some of the factors incorporated in risk

assessment.

· Level 5: The most advanced are

those that operate with full Automation vehicles that are fully autonomous and

can achieve this level of autonomy under all conditions without human

involvement. It is highly likely that liability, at least at this stage, will

fall almost entirely upon manufacturers and software providers. Instead,

insurers will focus on handling cyber liability, product liability and systemic

coverage for hacking or software errors.

2.2. Key technological advancements

Many

suites of cutting-edge technologies are critical for the functionality and

reliability of AVs. Artificial intelligence (AI) is the central piece which

powers decision-making, allowing vehicles to analyse camera, lidar, radar and

ultrasonic sensor data. Together, these components produce a seamless,

360-degree view of the vehicle's surroundings, detecting obstacles,

acknowledging potential movements and realizing real-time decisions.

From a

data sharing and sensing standpoint, the Internet of Things (IoT) is key to AVs

because it allows them to communicate with external systems, e.g. traffic

management infrastructure and other vehicles, to create a more interconnected,

intelligent transportation ecosystem. Moreover, machine learning algorithms

enable data to be collected in the operation as a source of a never-ending data

stream to improve driving performance continuously. Beyond that, V2X systems or

vehicles to everything, add dimension to safety: they allow vehicles and

infrastructure to communicate.

2.3. Predicted adoption timelines and market

penetration

Phase

adoption is expected due to the initial market penetration chiefly facilitated

by fleet operations, i.e. ride-sharing and logistics. Industry forecasts

indicate that market revenues will be led and driven by partially automated

vehicles (Levels 2 and 3), but adoption of Levels 4 and 5 will be significant

by the mid-2030s. A mix of technological readiness, regulatory alignment and

public trust will determine these timelines.

Adoption

will vary globally, with developed nations most likely to adopt first because

of the more mature infrastructure and better regulatory support. However, as AV

technology is more expensive and requires more building work for

infrastructure, emerging markets could experience delays. Increased adoption

will force industries to readjust from traditional vehicles to AVs as

generations pass, changing the landscape's risk and liability.

3.

Changes in Risk and Liability Frameworks

The rise

of autonomous vehicles (AVs) is turning conventional risk analysis and risk

management on its head. It then looks at how risk and liability frameworks have

evolved as vehicles8-12 have shifted

from human to technology-operated.

3.1. Traditional insurance risk models

This

traditional auto insurance is based on a risk-taking assessment that predicts

what is most likely to occur based on human drivers. Those factors include

driving history, age, location and the type of vehicle. It has always been

assumed that the causes of road accidents are human error beyond the 90 per

cent mark that exists globally; however, this is not always the truth.

Liability, therefore, usually rests with the driver, making the personal auto

insurance product the predominant offering in the market. Traditional models

have straightforward claims processes based on determining fault through driver

behaviour and environmental conditions. However, the arrival of the AVs

disrupts these models and moves the risk from the human drivers to the vehicle systems

and manufacturers.

3.2. Shifting liability: Driver vs.

Manufacturer vs. Software Provider

As more

and more driving tasks are transferred to AVs, there is a movement of liability

from people to organizations involved in designing, manufacturing and operating

the vehicles. Although less so in levels 2 and 3, a driver is still responsible

for monitoring and taking action if necessary. However, accountability becomes

more complex as vehicles move toward full autonomy (Levels 4 and 5).

In an AV

accident, the question arises: Does the fault result from a hardware error, a

software error or surrounding interference? Suppose, for instance, an AV

mistakenly misses an obstacle detectable by existing sensors because of a

sensor failure. The liability might lie with the manufacturer or vendor of that

sensor. Also, if a developer causes a software bug to crash, he can be held

responsible. Transforming driver liability into product liability disrupts such

frameworks and questions conventional insurance, prompting reinsurers to

consider products including manufacturer liability insurance and software

defect coverage.

3.3. Cybersecurity risks associated with

autonomous vehicles

AVs have

their Achilles heels: they rely on connectivity and the latest technology and

are susceptible to specific cybersecurity threats. The AV system can be the

target of cyberattacks that disrupt operations, steal sensitive data or allow a

cyber attacker to take remote control of the vehicle. In an interactive world

of cyber, such risks introduce an entirely new dimension of liability for the

insurer: the liability for the potential impact of a cyber incident on safety

and operational integrity.

A

coordinated hacking event targeting a fleet of AVs could inflict high harm. In

that context, liability may not lie with the vehicle owner, the software

provider or the network operator. To manage these risks, insurers must

incorporate cyber liability into their risk models and develop products

tailored for the loss they will see from attacks on AV systems.

The

development of the AV risk and liability framework shows the need for new

innovative insurance solutions. Standards around definition, the mitigation of

risks and a smooth transition to a future of autonomous vehicles will all

depend on the Collaboration of insurers, automakers and regulators.

4.

Implications for Property and Casualty Insurance

Panels

for Autonomous Vehicles (AVs) integration into the transportation landscape

will mark the beginning of the end of property and casualty (P&C) insurance

industry as we know it13-16. Insurers

must adapt to change the complexities introduced by AV technology, from

underwriting and claims management to the creation of new insurance products.

The image

depicts a conceptual architecture of a system of autonomous vehicle ecosystems,

P&C insurance frameworks, external factors such as regulations and

collaborations. Counting these domains apart clearly into blocks helps to see

how information runs and what dependencies are in the key components.

The

Autonomous Vehicles Ecosystem comprises the technological components defining

autonomous vehicles, including sensors, AI algorithms, decision systems,

communication systems and cybersecurity measures. Together, these components

permit autonomous vehicles to perform safely and efficiently. These

advancements in the field directly affect the shift in risk and liability,

resulting in new challenges for the insurance industry. P&C Insurance

Framework captures how the insurance industry is bearing these changes. This

framework is divided into three components: insurance products, data-driven

systems and risk models. New data sources are required as input for these risk

models, including underwriting, actuarial and claims management and the models

must adapt to new risks associated with autonomous technologies. Given the

risks inherent in autonomous vehicle operations, both insurance products have

cyber and product liability policies. Data-driven systems, particularly

telematics and analytics platforms, are key to collecting insights that power

the predictive analytics that feed into the risk model and product development.

The Legal and

regulatory block describes certain external forces that impact the autonomous

vehicles ecosystem and its framework of P&C insurance. The risk environment

is defined by compliance standards, liability framework and international

regulations that set up how insurers and manufacturers divide the

responsibilities (Figure 2). A sample is a safety system design wherein

liability is transferred from the drivers to the manufacturers and software

providers; this requires rethinking conventional insurance policies.

Figure

2:

Conceptual Architecture of Autonomous Vehicles and P&C Insurance

Interactions.

The final

block on the Collaboration highlights the necessity of automakers working with

technology companies and the government. The key to ensuring that these

technological developments map to regulatory requirements and to producing

insurance products that engineer the special risks of autonomous vehicles lies

with these collaborations. It depicts how such relationships encourage

innovation while paring risks and preserving consumer trust.

4.1. Changes in underwriting and pricing

Underwriting

has to pivot from human driver risk to technological and system risk in the AV

era. Security regulators and insurers must pay particular attention to the

reliability of AV hardware (sensors, cameras) and software (AI algorithms) and

how cyber-safe the insurance company and its manufacturers and suppliers are.

In

addition, pricing models will undergo major changes. Telematics, real-time

vehicle monitoring and data-driven insight will become more important than

traditional factors, such as driving history and behaviour. Further, it can

also mean accident frequency will decrease because of safer driving by AVs, but

because of the high cost of repairing advanced systems, claims costs may rise (Table

1).

Table

1:

Comparison of Traditional and AV Underwriting Factors.

|

Category |

Traditional

Vehicles |

Autonomous

Vehicles |

|

Risk Basis |

Driver behaviour, age, driving history |

Hardware/software reliability, cyber risks |

|

Claims Frequency |

High (human error) |

Low (technology-driven safety) |

|

Claims Severity |

Moderate |

High (cost of advanced technology) |

|

Pricing Data Sources |

Historical driver data |

Real-time telematics, manufacturer data |

4.2. Claims management in the era of autonomous

vehicles

As AVs

introduce new liability and fault determination challenges, the claims

management process becomes more difficult. Instead of blaming driver

negligence, insurers must investigate technological failures, software logs and

data from vehicle sensors. This necessitates Collaboration with manufacturers

and technology providers to access the proprietary data for claims resolution (Table

2).

Insurers

need to account for the further likelihood of disputes among several

participants, such as the vehicle owner, automaker and software developer.

Efficient claims processing will require advanced forensic capabilities and

specialized expertise in AV system design.

Table

2:

Traditional vs. AV Claims Management Processes.

|

Aspect |

Traditional

Vehicles |

Autonomous

Vehicles |

|

Fault Determination |

Based on driver behaviour |

Analysis of system logs and failures |

|

Primary Liability |

Driver |

Manufacturer, software developer or owner |

|

Claims Investigation Tools |

Police report, witness statements |

Telematics data, sensor logs, cyber forensics |

4.3. New insurance products and coverages

Because

of the transition to AVs, insurers must develop new products to tackle new

risks. Key new coverages include:

· Cyber liability insurance: It protects against

losses caused by cyberattacks on AV systems, such as data breaches, ransomware

and remote hijacks.

· Product liability insurance: Carriers of

manufacturers and software developers of AV components or algorithms that have

resulted in accidents due to defects.

· Technology error and omissions (E&O) insurance: Prepares products and

services offering appropriate error addresses against AV software and services,

generating liability claims.

· Fleet insurance for AVs: Designed to serve as tailored products

to companies operating AV fleets, which cover all coverage for all of their AV

system malfunctions and all of their liability risks (Table 3).

Table

3:

Examples of New Insurance Products for Avs.

|

Product |

Description |

Target

Audience |

|

Cyber Liability Insurance |

Covers risks from cyberattacks and data breaches |

Vehicle owners, fleet operators |

|

Product Liability Insurance |

Protects against claims from defective AV components |

Manufacturers, suppliers, developers |

|

Fleet Insurance |

Comprehensive coverage for AV fleets |

Ride-sharing companies, logistics firms |

|

Technology E&O Insurance |

Addresses liability for software or system errors |

Software developers, tech companies |

5.

Regulatory and Legal Considerations

Wherever

Autonomous Vehicles (AVs) are adopted, they drive significant changes in legal

and regulatory frameworks. Defining liability, guaranteeing public safety and

making17-20 certain insurance

implications associated with AV technologies are all critical to these changes.

5.1. Evolving legal frameworks for autonomous

vehicles

The

development of AV technology is leading governments to make new legal

frameworks that can govern how the technology's tests, deployments and

operations are conducted. Definition of manufacturers' roles and

responsibilities the definition of software developers' and owners' roles and

responsibilities are also defined as the key focus areas. Usually, such

regulations also prescribe system safety requirements, data transparency and

data cybersecurity.

For

example, in the United States, the National Highway Traffic Safety

Administration (NHTSA) has directed the AV developer to perform safety

assessments and report on safety as defined. Like the EU, the European Union

has established regulations regarding the legal approval of automated driving

systems, requiring such safety tests and data-sharing protocols.

Liability

issues are also being addressed by the legal framework, which will be put in

liability in the case of an accident taking place with an AV. Early legislative

efforts sound like a product liability trend in which manufacturers or software

providers might be responsible for system failures.

5.2.

International perspectives and regulatory disparities

Countries

differ widely in their approaches to regulating AVs and these vary

tremendously, ranging from what technological priorities countries are

pursuing, what legal traditions underpin some approaches to others and what

infrastructure readiness has prepared individual countries for.

· United states: There is little regulation, with federal

guidelines, essentially a broad framework and then states adopting their own

rules. California and Arizona are the leaders when it comes to regulating AV

testing.

· European union: Centralized safety and approval processes

dictating uniformity across member states is the EU's way of doing things.

· China: China has taken a government-led approach by implementing

a pro-AV development program and aggressive policies to increase AV testing in

innovative city environments.

· Emerging markets: Infrastructure limitations and resource

constraints create regulatory challenges to speed adoption in Latin America and

Africa.

5.3.

Impact of legislation on P&C insurance

The rules

of the P&C insurance industry are set into motion by legislation as the AV

environment unfolds. Insurers need regulatory clarity as to who is liable

before designing appropriate products. For example, if product liability laws

change, the focus of personal auto insurance could switch to policies that

cover manufacturers and software manufacturers, etc (Table 4).

Such

embedding of mandates for data sharing in regulations also affects claims

management. Insurers may require telematics data, crash reports and system logs

to determine faults in AV accidents. However, This data privacy is hampered by

laws preventing insurers from accessing it, such as the General Data Protection

Regulation (GDPR) in Europe, making the claims process difficult.

Table

4:

Legislative Impact on P&C Insurance.

|

Legislative Aspect |

Insurance Implications |

|

Liability

Frameworks |

Shift toward

product and cyber liability coverage |

|

Data Privacy

Laws |

Challenges in

accessing crash data for claims investigation |

|

Safety

Standards |

Influence on

underwriting based on compliance with safety regulations |

|

Cybersecurity

Requirements |

Increased

demand for cyber liability insurance |

6. Challenges and

Opportunities for Insurers

The

arrival of autonomous vehicles (AV) presents both challenging and new

opportunities for insurers. Change from human-driven to technology-driven

vehicles rewrites risk, liability and operational frameworks, thus requiring an

innovative path forward in Insurance.

6.1.

Data collection and privacy concerns

Autonomous

vehicle operations and the underwriting of insurance hinge on data. AVs are

likewise laden with sensors, cameras and telematics systems, which give

administrators data about vehicle performance, surrounding environments and

incidents. This data is extremely useful for insurers in assuring them of their

risks, the liability of the case and how they should price their policies.

However,

there are major privacy concerns associated with data collection. The General

Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy

Act (CCPA), for example, dictate how much data can be processed, stored and

even shared. They must balance these regulations while staying transparent and

protecting customer information. A big challenge is striking the right balance

between using data for underwriting purposes and keeping with the letter of

privacy regulations.

6.2.

Role of telematics and data-driven insurance models

In the AV

era of telematics, telematics is the cornerstone of data-driven insurance

models. Telematics, in this regard, collects real-time data on vehicle

performance and conditions to help uncover system reliability and see

operational patterns. It creates an opportunity for insurers to develop

usage-based Insurance (UBI) policies that calculate premiums based on actual

vehicle use and performance metrics and away from the static factors of vehicle

type and owner demographics.

Before an

incident, Telematics can also support claims management by providing objective

evidence from AV systems, such as speed, braking patterns and sensor inputs.

This data also improves accuracy in determining the fault and decreases

disputes throughout the claims process.

6.3.

Collaborations with automakers and technology companies

The

technology of AV is complex and requires the Collaboration of insurers,

automakers and technology companies. Insurers need to be extremely close to

automakers, learning about AV systems and their exact safety features,

limitations and how they fail. Detailed technical data is essential to

underwriting, pricing and claims management.

Insurers

have partnerships with technology companies, especially using artificial

intelligence and cybersecurity, which can enable insurers to stay on top of

emerging risks in the industry. This can extend to joint initiatives to enhance

AV cybersecurity that reduce the risk of hacking or data breaches, thus making

for safer vehicle operations. In addition, collaborations foster innovation in

the insurance product, such as bundled offers, including automakers offering

insurance coverage as part of the sale or lease agreement with the vehicle.

7. Preparing for the

Future: Strategies for Insurers

Insurers

must adopt forward-looking strategies to thrive in a quickly evolving land space

defined by autonomous vehicles (AVs). This section looks at innovations, risk

modelling and consumer trust around the issue of the future.

7.1.

Investing in innovation and technology

In order

to go from traditional cars to AVs, insurers will need to understand the

technology and innovate. To improve their ability to assess risks with

complicated AV systems, insurers must begin investing in AI, machine learning

and big data analytics. Telematics, blockchain and the Internet of Things can

all be rolled into a live claims process, fraud detection and the ability to

monitor the performance of AV in real-time.

In

addition, insurers must participate with tech companies and automakers to

develop solutions that best meet the special requirements of AV drivers and

operators. Insurance cases are a prime use case for such an integrated platform

where insurers can seamlessly integrate their platforms with AV systems for

instant insurance activation, real-time risk updates and immediate claims

resolution.

7.2.

Risk modelling and predictive analytics

Risk

modelling is essential for understanding and managing the new types of risks

brought by AVs. Insurers can use predictive analytics to gauge the performance

of AV hardware and software and estimate the probability of accidents, as well

as what a system failure could cost an insurer.

Insurers

can use machine learning algorithms to build more accurate risk models using AV

testing, telematics and incident report data. Such models can depend on weather

conditions, other urban or rural factors and cybersecurity complexity. This

also helps insurers provide bespoke policies for particular customers with

regard to which AV types, manufacturers or usage patterns they use.

7.3.

Building consumer trust in autonomous vehicle insurance

The

insurance industry is built on the consumer's trust, a cornerstone that must be

rebuilt as trust builds in managing emerging risks. There must be clear lines

of communication on how AV insurance works, what it covers and how premiums are

calculated. Insurers can handle the complexities of AV liability, data

security, claims, etc. And consumers need to understand this.

In

particular, data privacy issues are extremely well-suited for transparency

objectives. Insurers need to reassure policyholders that their personal and

vehicle data are used responsibly and that they are following legal standards.

It can also help consumers stay confident in their purchase decisions and

appeal to broader customers, offering flexible and easy-to-understand policies

like pay-as-you-drive or bundled coverage when an AV is purchased.

8. The Impact of

Autonomous Vehicles on P&C Insurance: Preparing for the Next Frontier of

Risk and Liability

Great

changes in the property and casualty (P&C) insurance landscape will be

brought about through the rise of autonomous vehicles (AVs). Insurers will have

to adjust to new risks, liabilities and coverage needs arising from this shift

to AV as they rise from experimental technology to mainstream deployment. In

this section, the future of the insurance market is anticipated, especially in

commercial auto insurance, workers' compensation and cyber liability, as well

as the challenges and opportunities that insurers have to be ahead of the

curve.

8.1.

Shifts in insurance premiums and coverage needs

The

adoption of autonomous trucks and vehicles is expected to create notable

changes in several key areas of Insurance:

·Commercial auto insurance: The rise of AVs could

be extremely damaging to this segment by definition, having traditionally been

the most loss-ridden. Reducing the frequency of claims and the number of

accidents could be achieved by eliminating human error, which causes nearly 94%

of traffic accidents. Thus, the premium for commercial autonomous vehicles will

begin to decline. However, these new risks will include software malfunctions,

cyberattacks and product liability issues caused by autonomous systems. So,

these risks will make underwriting more complicated; insurers will need to

create more sophisticated models than just intuiting based on data; for

commercial auto insurers, offering even a shift of 20% of their premiums to

other lines of coverage could result in an annual loss of premiums over $7

billion.

· Workers' compensation: The adoption of AV can greatly reduce

workers' compensation claims related to driving. However, with AVs assuming the

driving task, the number of occupational accidents and fatalities to human

drivers would probably decrease. It could help profitability for workers' comp

insurers. However, as AVs do away with jobs currently protected under workers'

compensation for drivers like truckers and delivery persons, insurers could

lose premium revenue. One estimate for the annual premium loss from this

segment is $3 billion.

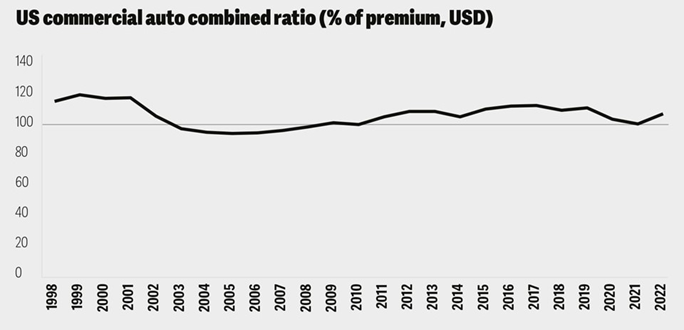

8.2.

Trends in US commercial auto combined ratio

The US

commercial auto insurance business trend between 1998 and 2022 is expressed as

a visual fraction. The combined ratio is a metric in the insurance world used

by the industry to measure underwriting profit and is expressed as a percentage

of premiums. A combined ratio below 100% is underwriting profit (above 100%

indicates loss).

It is

apparent from the graph that the return on investment, known as the combined

ratio, for commercial auto insurance has endured underwriting losses over the

years, usually above 100 percent, which usually implies an unsaturated appetite

on the part of the insurance buyers. The tone of this trend speaks to insurers'

plight in this niche market, where the high fly rate of claims from human error

in driving is the root of most accidents. However, the ratio can indicate a few

relatively win-overs in the loss-making sector, such as the early 2000s and

around 2013.

Automated

vehicles will decrease human participation in driving, which is expected to

greatly diminish human error frequency and severity of accidents. Such a change

could result in a better-combined ratio on commercial auto insurance. However,

the image also points to how volatile this metric is. Insurers must guard

against new risks, like software glitches and cyber-attacks, which will temper

the gains they expect.

The graph

offers a compelling basis for the argument that, from a commercial auto point

of view, autonomous vehicles have the potential to fundamentally alter a

long-term trend. Through historical performance context and AV adoption's

expected impact on risk and liability, insurers can better anticipate and

prepare for the paradigm shift in risk and liability.

· Cyber liability insurance: As AVs become more

connected with increasingly high reliance on advanced, sophisticated software,

including an estimated 100 million lines of code in a single vehicle, their

cyber vulnerabilities will increase. Hacking, data breaches and system failures

may disrupt vehicle operations, resulting in accidents and damage to critical

infrastructure. Developing specialized cyber liability products with complete

cyber coverage for AVs' fairly interconnected nature will become necessary to

ensure insurers adapt to this vertical. That will mean insurance coverage for

data breaches, software vulnerabilities and the legal liability stemming from

attacks on AV systems using cyber (Figure 3).

Figure

3: US Commercial

Auto Combined Ratio.

8.3.

Challenges in underwriting and risk assessment

The

transition to AVs presents significant challenges for insurers, particularly in

underwriting and risk assessment:

·Lack of historical data: Autonomous vehicles have little

historical data. Unlike traditional vehicles, which have decades of accident

data from which to underwrite risk models, insurers want to ensure AVs are as

safe as manually driven cars to drive down costs. However, unless they have

access to large troves of data, ensuring them accurately while understanding

the actual risks of being involved in accidents is nearly impossible. This

means that insurers may have to innovate in new ways, using telematics data and

almost real-time monitoring of AVs to learn. The lack of permanence in services

required and the nature of the risks in this business make it, in a sense,

similar to the situation that the cyber insurance industry is undergoing:

insurers are evolving their models as new risks become apparent.

Complex liability issues: Accidents involving AVs will probably

be tough to prove fault in. It could be shared between several parties (vehicle

manufacturer, software provider or a third-party service provider), making the

claims process more intricate. It's not always clear that the person steering

or braking solely caused an accident. Sometimes software bugs, GPS errors and

external factors like potholes could all be contributing to an accident that

makes it difficult to assign fault. To set the right framework for AV, insurers

will have to find new tools and methodologies for investigating and determining

liability for AV-related claims. As AV litigation increases because parties try

to establish clearly defined fault and liability, this complexity may lead to more

litigation in AV-related accidents.

· Regulatory hurdles: Because autonomous vehicles are still a

relatively new technology, they are being adopted into a regulatory environment

that is also evolving. Some states or countries have approved AV testing and

use, but a uniform global regulatory framework has not yet been established. AV

insurers will have to figure out how to travel transportation by machine along

a confusing mosaic of local and state regulations that differ on safety

requirements, testing rules and liability. However, AVs will also need federal or

global regulatory approval to operate in an interstate or international market,

increasing complexity for insurers wanting to operate in different markets.

8.4.

Strategic adaptation for insurers

To

prepare for the impact of autonomous vehicles on the insurance landscape,

insurers should consider several strategic approaches:

· Partnerships with manufacturers: Insurers have to build

relationships with autonomous vehicle manufacturers to know how the technology

works, the safety features and the potential risks. Manufacturers like Tesla or

Waymo will partner with insurers to gain access to technical data, vehicle

performance insights and system reliability metrics to underwrite, risk model

and manage claims. As with emerging risks we've discussed, companies like

Liberty Mutual are already working with AV manufacturers to be ready to meet

the risks coming down the pike. Through these collaborations, insurers can

leverage the unique AV needs to work with them to develop policy.

· Innovative coverage solutions: However, the new risks

and liabilities of AVs require insurers to create innovative and flexible

coverage solutions. For example, customizable policies that can suit the

different needs of the diverse set of players in the AV ecosystem (vehicle

manufacturers, fleet operators and software developers) will be important.

Bundled or customizable policies for autonomous vehicles, for example, which

might combine aspects of the risks posed by product defects with the risks

associated with cyberattacks, are already being explored by companies such as

AXA XL. These hybrid policies enable insurers to provide both traditional

vehicle risks and new AV-specific exposures.

· Proactive risk management: Insurers should fund

research and development in AV-specific risk management strategies. Insurers

can best address new risks by introducing products pre-emptively to better

anticipate and address emerging risks. Participating with the broader AV

ecosystem will put insurers at the forefront of adapting to address new ones

and give them a competitive advantage. It will allow insurers to be proactive

and leaders in the industry, ensuring innovation as we continue to see AV

adoption grow.

9. Conclusion

The

entrance of Autonomous Vehicles (AVs) into the property and casualty (P&C)

insurance industry is a transformative change that adds challenges and

opportunities. The Keys to adapting to AVs' evolving risk landscape are as AVs

evolve from cutting-edge to mainstream vehicles. However, by eliminating human

error, traditional vehicle-related claims will likely decrease in frequency and

reduce rates, whereas new risks will emerge, including cyber threats, software

malfunctions and product liability. These risks demand an overhaul of the

insurers' underwriting, pricing and claims management strategies through

advanced technologies and fresh data sources.

Finally,

complexity will mount for the insurers to face liability issues tied to

AV-related accidents where the fault will be increasingly hard to pin down.

However, the claims process itself will be more complicated, with multiple

parties possibly sharing the responsibility, including manufacturers, software

providers and even third-party service operators. In addition, the AV's

regulatory environment is still being developed and the insurers are currently

facing different national and regional regulations to adapt to. Insurers must

stay ahead of regulatory change to be competitive and mitigate risk.

However,

despite these challenges, P&C insurance has never been more promising

regarding the future of Insurance in an AV-driven world. Investing in

innovation and technology will enable insurers to build enhanced risk

assessment models utilizing telematics data and to build more targeted coverage

solutions that will assist AV stakeholder's needs. Insurers can then use

insights from collaborations with automakers and technology companies to offer

new, different, more tailored insurance products designed for that evolving AV

landscape. Additionally, insurers who can facilitate the building of consumer

trust in the new options for coverage will have a considerable advantage across

AVs' increasing presence.

Ultimately,

autonomous vehicles will greatly change the insurance industry and innovations,

flexibility and proactive risk management will be required. Those insurers who

lean in and make investments in these new technologies and strategies will not

only ride the AV curve but emerge as leaders in a fast-changing landscape. A

successful future will be one of toggling emerging risks and opportunities,

accommodating the insurers' needs and the future of consumers and ensuring the

resilience of the insurance sector to change.

10. Author Contribution Statement

Sateesh Reddy Adavelli,

Solution Architect, USA

Led the

conceptual framework development for the paper, focusing on AV impact across

insurance models. He was the primary contributor to the risk and liability

frameworks section, drawing on his extensive experience in insurance

architecture. Sateesh developed the conceptual architecture diagram showing AV

and P&C insurance interactions and provided valuable insights on

international regulatory disparities. He was instrumental in formulating

strategic recommendations for insurers and ensuring cohesive integration of all

sections.

Ravi Teja Madhala,

Sr Software Developer Analyst, USA

Brought technical

depth to the paper through his analysis of AV technologies and their

implementation timelines. Ravi's expertise in cybersecurity formed the backbone

of the sections addressing cyber risks in autonomous vehicles. He conducted

research and developed the comparative analysis between traditional and AV

underwriting factors, compiled the US Commercial Auto Combined Ratio data and

provided critical insights on telematics and data-driven insurance models. His

contributions were especially valuable in identifying technical challenges in

AV risk assessment.

Nivedita Rahul,

Business Architecture Manager, USA

Provided crucial business perspective through her analysis of P&C insurance implications. Nivedita led the research on emerging insurance products and coverages for AVs and developed the claims management transition framework. Her expertise in data privacy and regulatory compliance strengthened multiple sections of the paper. She analyzed business impacts for insurers and contributed significant insights on consumer trust development in AV insurance products. Nivedita's business strategy expertise helped shape the paper's recommendations for industry preparation.

All three authors

collaborated throughout the research and writing process, bringing together

their complementary expertise in insurance architecture, technical

implementation and business strategy to create a comprehensive analysis of how

autonomous vehicles will transform the property and casualty insurance

landscape.

11. References

- Tarr JA, Tarr AA. Autonomous Vehicles: Liability and

Insurance. In The Global Insurance Market and Change. Informa Law from

Routledge, 2024: 157-181.

- Faisal A, Kamruzzaman M, Yigitcanlar T, Currie G.

Understanding autonomous vehicles. Journal of transport and land use, 2019;12: 45-72.

- Kewal T,

Saxena C. Digital Disruption in Insurance Value. Innovative Computing and

Communications: Proceedings of ICICC 2024, Volume, 2024;5: 173.

- Weiser PJ. Regulatory challenges and models of

regulation. J on Telecomm High Tech L, 2003;2.

- Leenes R, Palmerini E,

Koops BJ, et al. Regulatory challenges of

robotics: some guidelines for addressing legal and ethical issues. Law,

Innovation and Technology, 2017;9: 1-44.

- Brawley A, Kwok D, Lesarge J, Nickerson E. Promoting

Competition in P&C Insurance, 2021.

- Woo

S, Youtie J, Ott I, Scheu F. Understanding the long-term emergence of

autonomous vehicle technologies. Technological Forecasting and Social Change, 2021;170:

120852.

- Schoettle B, Sivak M. Motorists' preferences for

different levels of vehicle automation. University of Michigan, Ann Arbor,

Transportation Research Institute, 2015.

- Cascetta E, Carteni

A, Di Francesco L. Do autonomous vehicles

drive like humans? A Turing approach and an application to SAE automation Level

2 cars. Transportation research part C: emerging technologies, 2022;134: 103499.

- Stayton E, Stilgoe J. It's time to rethink levels of

automation for self-driving vehicles [opinion]. IEEE Technology and Society

Magazine, 2020;39: 13-19.

- Rustad ML. Product Liability for Software Defects in

Driverless Cars. S Cal Interdisc LJ 2022;32: 171.

- Sun X, Yu FR, Zhang P. A survey on cyber-security of connected and

autonomous vehicles (CAVs). IEEE Transactions on Intelligent Transportation

Systems, 2021;23: 6240-6259.

- Taeihagh A, Lim HSM. Governing autonomous vehicles:

emerging responses for safety, liability, privacy, cybersecurity and industry

risks. Transport reviews, 2019;39: 103-128.

- Kim K, Kim JS, Jeong S, et al. Cybersecurity for

autonomous vehicles: Review of attacks and defence. Computers &Security, 2021;103:

102150.

- Esho

N, Kirievsky A, Ward D, Zurbruegg R. Law and the determinants of property‐casualty insurance.

Journal of Risk and Insurance, 2004;71: 265-283.

- Hanweck GA, Hogan AM. The structure of the

property/casualty insurance industry. Journal of Economics and Business, 1996;48:

141-155.

- Pütz F. The impact of connected automated vehicles on

the insurance sector: a comprehensive analysis of legal and risk factors

(Doctoral dissertation, University of Limerick), 2019.

- Garikapati D, Shetiya SS. Autonomous Vehicles: Evolution of Artificial

Intelligence and Learning Algorithms, 2024.

- Ryan C. Driverless cars: Preparing for the impact on the automobile insurance industry, 2017.

- Channon M, Marson J. THE liability for cybersecurity

breaches of connected and autonomous vehicles. Computer Law & Security

Review, 2021;43: 105628.